CORPORATE GOVERNANCE

The Board sets strategy and provides oversight and control, acting as an independent check and balance to the Senior Management Team, whose responsibility it is to run the business

Our Role is to:

Dear Stakeholder,

I am pleased to present our Corporate Governance Report for 2017.

The Bank aspires to the highest standards of corporate governance and ethical conduct. Doing what we say, reporting results with accuracy and transparency, and maintaining full compliance with the laws, rules and regulations is integral to the way we govern the Bank's business operations.

The Corporate Governance Report illustrates the important areas of the governance framework of the Bank. This report covers the “Factual Finding Report” submitted by the External Auditors in relation to compliance with the Corporate Governance Directions issued by the Central Bank of Sri Lanka (CBSL).

As required by the Code of Best Practice on Corporate Governance issued jointly by the Securities and Exchange Commission of Sri Lanka and the Institute of Chartered Accountants of Sri Lanka in 2013, we hereby confirm that, we are not aware of any material violations of any of the provisions of the Code of Business Conduct and Ethics (as embodied in the internal Code of Corporate Governance applicable to directors and key management personnel of the Bank as the case may be) by any director or key management personnel of the Bank.

We pride ourselves on upholding the spirit of Corporate Governance regulations and best practices beyond merely ticking the boxes. Please find a detailed description of our compliance with these regulations and best practices on pages 220 to 254 of this Report.

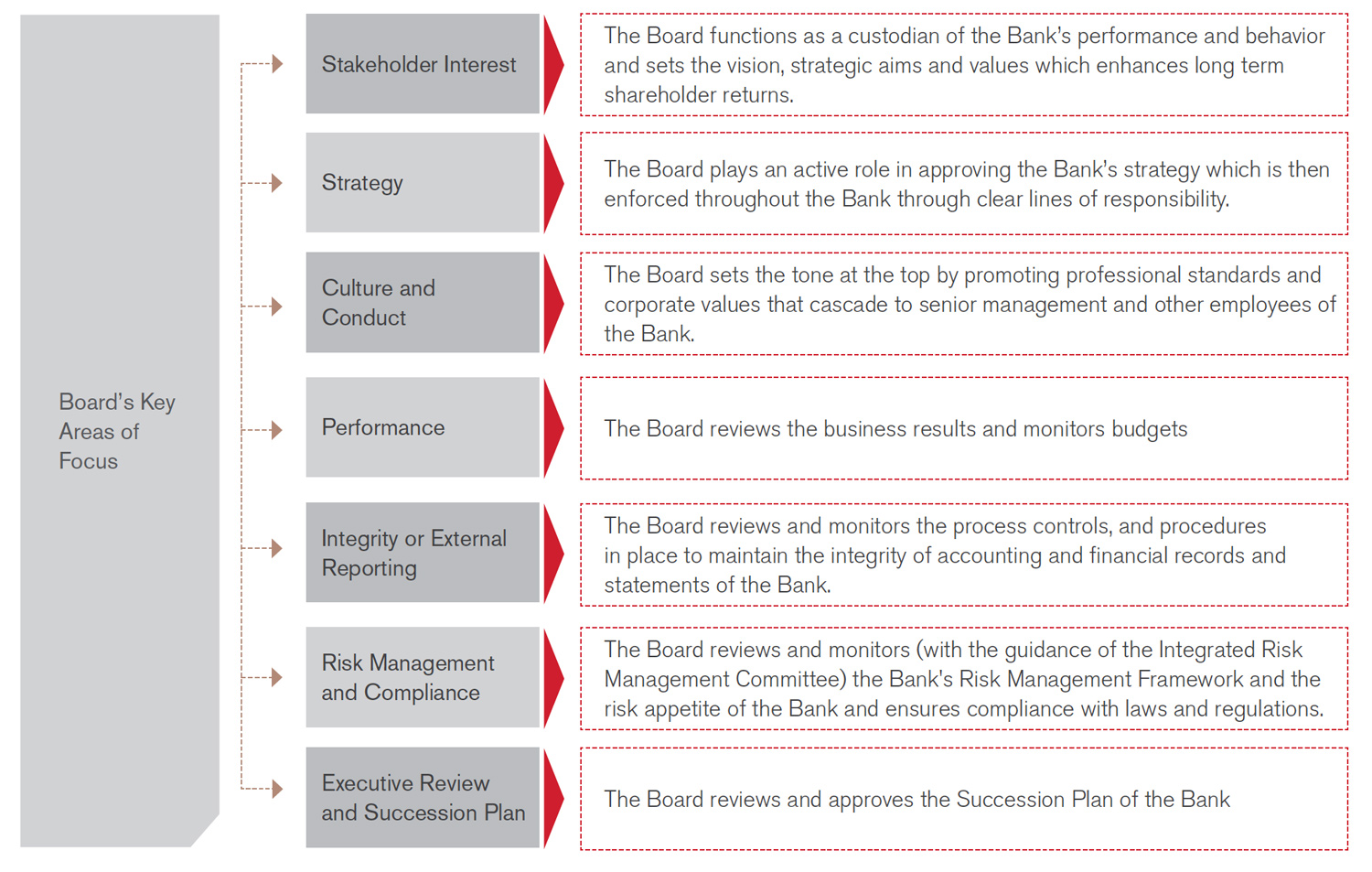

Our key priority as a Board is to build a sustainable business that generates good returns for our stakeholders over the longterm. Our role is to set NDB’s strategy, provide leadership and create a culture that helps achieve our strategy, ensure effective execution by monitoring performance and above all, make sure that risk is managed appropriately.

Strategic Direction

As Chairman, I ensure that sufficient time is set aside at Board meetings for open and constructive discussion of significant issues, most importantly, strategy. In 2017, critical progress was made in setting the foundation for sustainable long term success with the launch of the Bank’s new strategic initiative called “Transformation 2020”. The Board provided oversight of senior management in developing this strategy and will continue to provide support in ensuring that the key strategies are delivered in a timely manner.

Further in 2017, a Board Credit Committee was established to ensure that more time of the Board can be spent on the discussion of strategy, performance, business opportunities and the management of key risks.

Right Culture

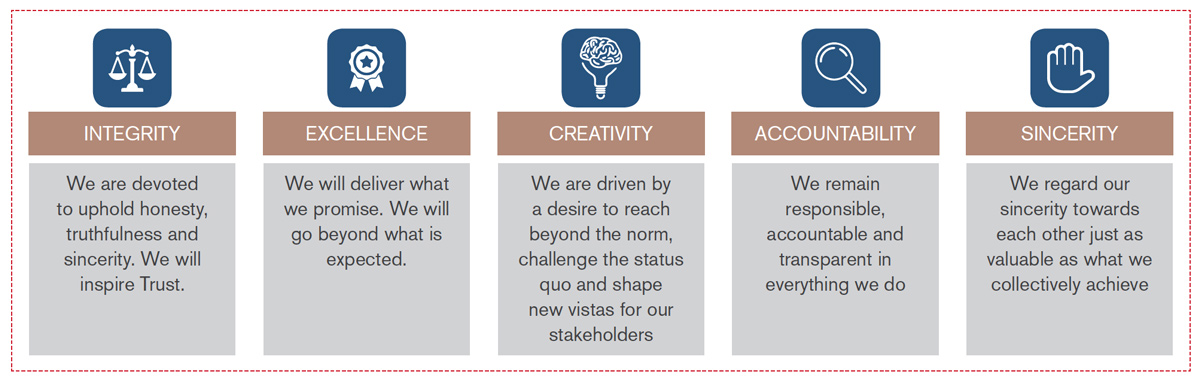

How we do things is just as important as what we do. The Board plays an important role in setting the tone and creating a culture that will ultimately deliver sustainable success. Effective governance is therefore not simply about having a framework or processes in place, it is about people and how they interact. In this transformational journey we are focusing not only on what we do but on how we do it, and are committed to embedding a values-driven culture at NDB, one where we are expecting every member of the NDB family to demonstrate the values of Integrity, Excellence, Creativity, Accountability and Sincerity when interacting with our colleagues, customers, suppliers, shareholders and society.

Monitoring Performance

A dedicated project management office and project steering committee consisting of members of the Board, senior management and senior representatives of the IFC advisory team was established to provide the vital leadership to monitor and track the strategic transformation initiative. The Board’s focus is now on execution and supporting the senior management team to achieve its strategic goals and is regularly updated on progress made.

Management of Risk and Control

Our Board subcommittees play a vital role in providing oversight of risk management and ensuring that our risk appetite and risk profile are consistent with and support our strategy to deliver long-term, sustainable success. Our internal controls cover financial, operational, compliance, technology controls, as well as risk management policies and systems.

In 2017, the Bank achieved a new milestone in our corporate governance journey when our Corporate Governance Report in the 2016 Annual Report won the Gold Award at the Chartered Accountants Annual Reports Awards 2016 thereby recognizing our goal to transparency and reporting on a wide range of financial and non-financial obligations to ensure our accountability.

Our commitment to strong and effective governance continues and we believe that this will help create value for multiple stakeholders, including our shareholders. We invite you to take a closer look at our governance initiatives and practices during the year 2017!

A W Atukorala

Chairman

CORPORATE GOVERNANCE INITIATIVES FOR THE YEAR 2017

In order to ensure that all governance related matters receive the focused attention of the full Board, the Corporate Governance and Legal Affairs (CGLA) Committee was dissolved and such matters were brought under the purview of the Board. Further, matters relating to legal risk and conduct risk which came within the scope of the CGLA was incorporated into the TOR of the Integrated Risk Management Committee which provides oversight on risk management. |

A Credit Committee was established to review credit and approve credit proposals coming under the Committee’s Delegated Level of Authority and recommend (when required) proposals to the Board. By doing so the Board has more time to focus on areas such as strategy, corporate governance, performance, business opportunities, management of key risks etc. |

In order to ensure smooth and effective execution of the Bank’s strategic initiative "Transformation 2020", a Project Steering Committee and a dedicated Project Management Office (PMO) was established to monitor and manage the Bank’s strategy program. |

A T20 website was launched to share progress made on achieving the objectives set out in the Bank's strategic plan and to ensure that all employees are kept informed of progress made under this initiative. |

A series of outreach and organizational change management workshops were held across all regions to drive and entrench the Bank's Corporate values and the "One NDB" culture with each member of the NDB Family. |

All TORs, Policies, Procedures and Product Program Guides are tracked on a monthly basis to ensure that they are reviewed in a timely manner and are updated in line with new regulations and best practices. |

A share trading black out period was introduced on the NDB Share for all directors and all employees of the Bank. This ensures that directors and employees do not trade based on any price sensitive information they may possess. Further, to ensure that there is no speculative trading on the NDB Share, a minimum holding requirement was also introduced. All share trades carried out by employees of the Bank are monitored to ensure compliance. |

All documents pertaining to Board and subcommittee meetings were made available in electronic format on the tablets provided to all directors. Further, to support directors to keep abreast with the changing regulatory landscape, all laws and regulations relating to banking business are uploaded in electronic format on their tablets. |

Training Programs on “Anti-Money Laundering Regulations, AML trends and industry best practices” and “IFRS 9 and the implications to the Bank” were conducted for the entire Board during 2017. This is in addition to directors training programs attended by individual Board members. |

A new E Learning Module on Anti Money Laundering and Terrorist Financing in line with new regulations issued by the regulator was launched in 2017. Completion of the training and passing the assessment was mandatory for all employees of the Bank. 1950 employees of the Bank have completed the training and passed the assessment in 2017. |

A Fraud Risk Management Policy was approved by the Board in 2017 establishing a framework within which the fraud risk of the Bank is to be managed. The policy details the tools and techniques that are to be implemented to manage fraud risk within the Bank in a standardized manner. |

The Board, all subcommittees and management committees carried out self-assessments to critically evaluate the effectiveness of the Board and each of the committees. The results of the self-evaluations were discussed and areas for improvement together with an action plan was mandated. |

OUR GOVERNANCE FRAMEWORK

We have a clearly defined governance framework that promotes transparency, fairness and accountability.

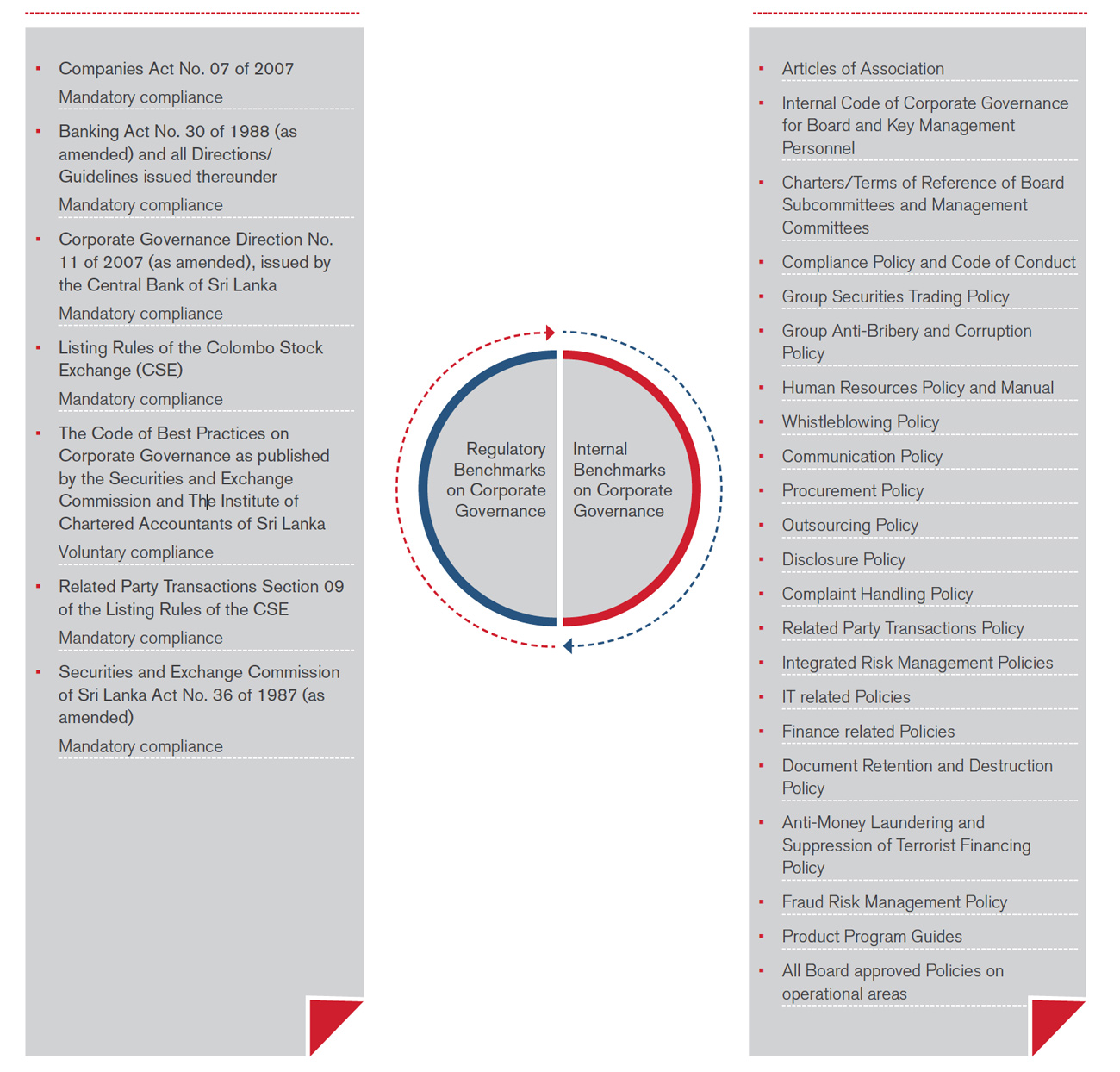

Our governance framework is anchored on (a) competent leadership, (b) creating the right culture and values, (c) effective risk management and controls and (d) regular engagement with our stakeholders.

The internal and external regulations that strengthen the Bank’s Corporate Governance Framework are as follows:

THE BANK’S GOVERNANCE FRAMEWORK

COMPETENT LEADERSHIP

The Board provides challenge, oversight and advice to ensure that we are doing the right things in the right way.

The Board requires the right balance of expertise, skills, experience and perspectives to be effective. It also needs to have the right information, at the right time, so that it can engage deeply on how the business is operating, how the Senior Management Team is performing and fully understand the risks and major challenges the business is facing.

The performance of the Board, the Board subcommittees and the directors is evaluated each year with the Board Performance Evaluation Process.

BOARD COMPOSITION

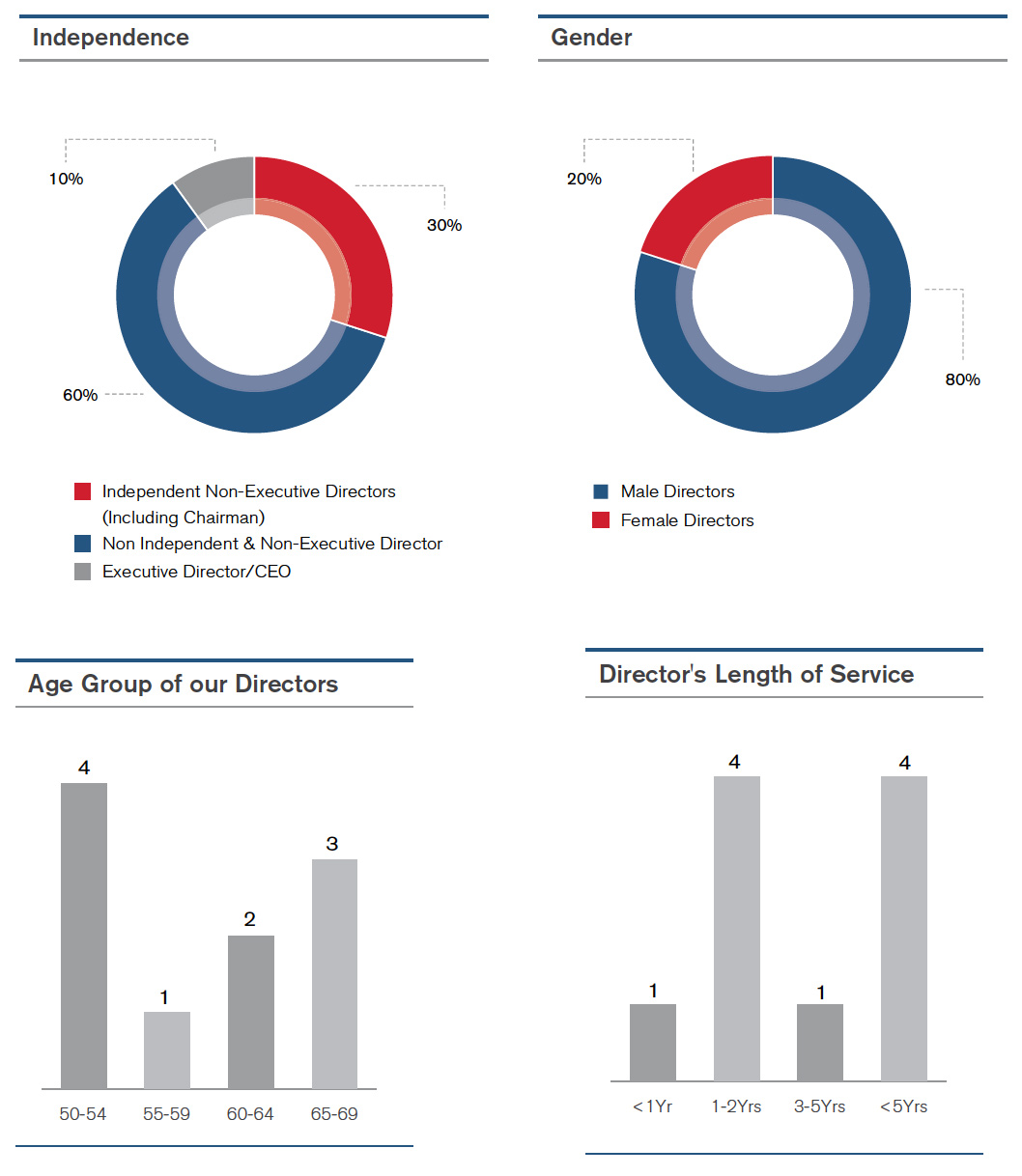

Our Board members have a broad range of expertise and brings skills and experience from a diverse range of backgrounds, including sufficient skills and experience appropriate to the Bank. The tenure of our directors demonstrates a good balance between continuity and fresh perspectives. The size and composition of the Board is appropriate given the current size and footprint of the Group’s operations. The make-up of our Board reflects diversity of gender. The CEO is the only executive director on the Board. The independence of non-executive directors is reviewed on an annual basis as part of the directors’ evaluation process, taking into account length of tenure and any relationships that might be considered as factors when determining independence. The proportion of independent non-executive directors on the Board (six out of ten) is high thereby bringing unbiased judgment in decision making.

BOARD OF DIRECTORS' INDUSTRY/BACKGROUND EXPERIENCE

Industry Experience |

No of Directors |

Banking |

5 |

Finance |

3 |

Entrepreneurship |

1 |

Insurance |

3 |

Law |

2 |

Public Policy & Public Administration |

2 |

IT |

1 |

Investment Banking |

1 |

Media |

2 |

WHERE TO FIND INFORMATION ON EACH DIRECTOR?

Information on the Director’s profiles can be found on pages 188 to 197 The gender balance, age balance, expertise and length of service are depicted in graphical form on page 212. The information on independence status, date of appointment, length of service and Board meeting attendance is detailed in the table below. Information relating to directors’ appointments in Board subcommittees and attendance at subcommittee meetings is found on page 216.

THE STRUCTURE, COMPOSITION AND ATTENDANCE OF THE BOARD AS AT 31 DECEMBER 2017

Name of Director |

Areas of Expertise |

Independent / Non Independent under CBSL Direction |

Independent / Non Independent under ICASL/ SEC Code Direction |

Date of Appointment |

No of Meetings Eligible to Attend |

No of Meetings Attended |

Mr. A W Atukorala (Chairman) |

Management and Banking |

Independent |

Independent |

31.08.2016 |

14 |

14 |

Mr. A. K Pathirage (Deputy Chairman) |

Retail Trade, Insurance and Entrepreneurship |

Non Independent |

Non Independent |

18.02.2011 |

14 |

14 |

Mr. P L D N Seneviratne |

Banking, Finance and Management |

Non Independent |

Non Independent |

01.01.2017 |

14 |

14 |

Mr. T L F Jayasekara |

Accounting, Banking and Textile Industries |

Independent |

Independent |

10.02.2010 |

14 |

13 |

Mr. D S P Wikramanayake |

Accounting, Banking, Insurance and Investment Banking |

Non Independent |

Non Independent |

04.06.2010 |

14 |

14 |

Mrs. Kimarli Fernando |

Law, Banking and Management |

Independent |

Independent |

04.06.2010 |

14 |

13 |

Mrs. Indrani Sugathadasa |

Management, Insurance, Public Administration, Plantations and HR |

Independent |

Independent |

04.10.2013 |

14 |

14 |

Mrs. D M A Harasgama (resigned w.e.f 30th June 2017) |

Finance, Public Policy and Management |

Non Independent |

Independent |

22.04.2015 |

8 |

8 |

Mr. D M R Phillips PC |

Law |

Independent |

Independent |

22.04.2015 |

14 |

14 |

Mr. K D W Ratnayaka |

Management, IT and Media |

Independent |

Independent |

13.05.2015 |

14 |

13 |

Mr. N S Welikala (Resigned w.e.f. 30th April 2017) |

Banking, Finance and Management |

Independent |

Independent |

11.10.2016 |

6 |

6 |

Mr. R. Semasinghe (appointed w.e.f 26th September 2017) |

Public Policy, Media and Management |

Non Independent |

Independent |

26.09.2017 |

3 |

3 |

BOARD MEETINGS |

|

Prior to Board Meetings |

During Board Meetings |

• All Board meetings are scheduled and informed to the Board at the beginning of each calendar year to provide directors an opportunity to attend |

• The Chairman encourages and facilitates constructive dialogue during Board meetings |

• All directors are given an opportunity to include matters and proposals in the agenda for Board meetings if required |

• Board members come well prepared and engage in robust discussions on key matters pertaining to the Bank |

• The Chairman draws up the agenda in consultation with the Chief Executive Officer and Company Secretary to ensure that there is sufficient information and time to address all agenda items |

• The Chairpersons of Board subcommittees provide detailed updates to the Board on key decisions taken at subcommittee meetings and any areas of concern |

• Formal notice of meetings, the agenda and Board papers related to each Board meeting are circulated at least 7 days in advance of the Board meeting. These documents are uploaded through a secure connection to the tablets of all directors in order to ensure that Board members have access to complete information prior to Board meetings |

• CEO prepares complete and accurate financial statements and disclosures in accordance with the financial reporting standards which illustrates a fair view of the Bank's performance |

• Directors can participate by telephone or video conference |

• If a director of the Bank has a conflict of interest in a matter to be considered by the Board, such matters are disclosed and discussed at the Board meetings, where independent non-executive directors who have no material interest in the transaction, are present. The relevant director excuses himself from the meeting when such matter is being considered by the Board and does not participate in the discussion and decision |

• Directors have the discretion to engage external advisers |

• The Board minutes contain adequate details appropriate to the matters dealt with during Board meetings. All directors bring their independent judgment to matters discussed at Board meetings. Dissenting views are also duly recorded in the Board minutes in detail |

Effective Engagement with the Board |

|

• The Board is regularly updated on Board performance, progress against strategy, key risks and control lapses that have been identified. • Directors have access to Senior Management and request for additional information whenever required to make informed decisions. • Senior Management make regular presentations to the Board on matters under their purview and are also called in by the Board to explain matters relating to their respective areas. • Directors had the opportunity to interact with The Leadership Team at a specially hosted evening cocktail. • Directors have independent access to the Company Secretary at all times. The Company Secretary attends all Board meetings and generally assists directors in the discharge of their duties. • As some directors sit on the Boards of subsidiaries in the Group this arrangement gives the Board access to first hand insight on the activities of the subsidiaries. • All laws and regulations issued that relate to banking business are uploaded to the tablets provided to directors together with an explanatory note to support directors to keep abreast with the changing regulatory landscape. |

|

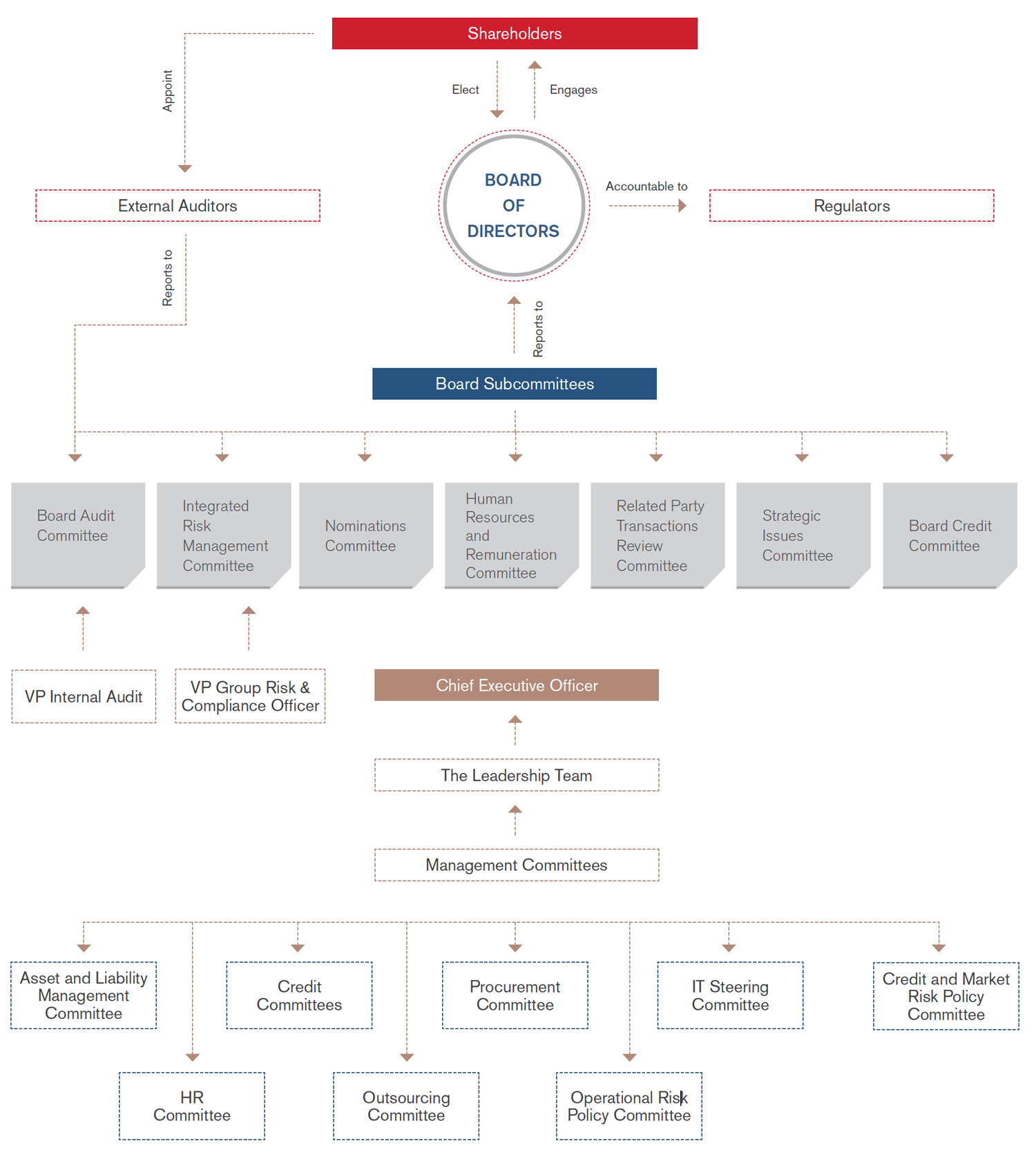

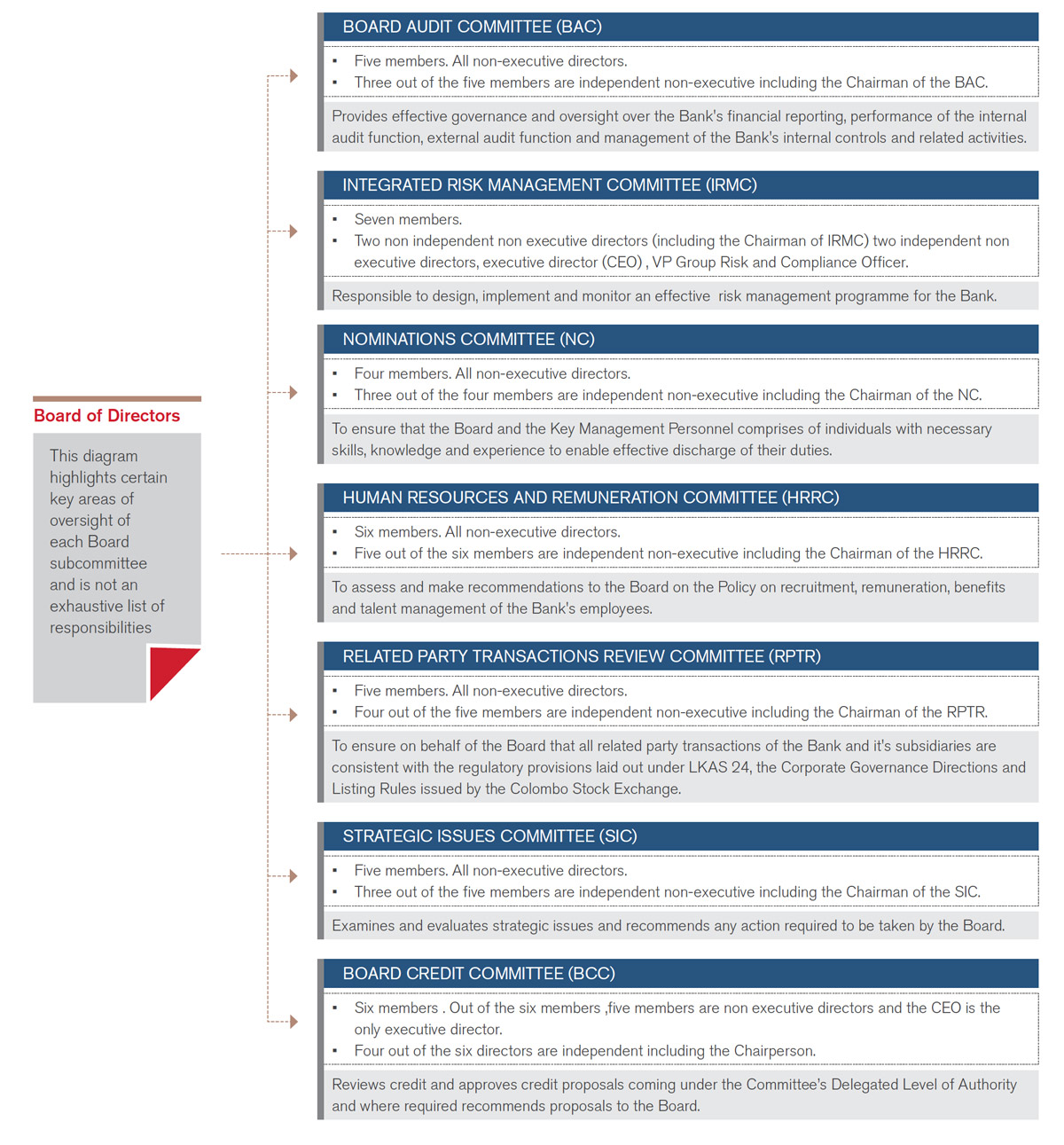

BOARD SUBCOMMITTEES

To discharge its stewardship and fiduciary responsibilities effectively, the Board delegates authority to Board subcommittees to enable directors forming part of respective committees to focus on their designated areas of responsibility and impart knowledge in areas where they have expertise. This empowers the Board to provide effective oversight and leadership and focus on key issues and prioritize its time and resources.

DETAILS OF MEMBERS OF THE BOARD SUBCOMMITTEES AS AT 31 DECEMBER 2017

Name of Subcommittee |

Human Resources and Remuneration Committee |

Integrated Risk Management Committee |

Nominations Committee |

Board Audit Committee |

Related Party Transactions Review Committee |

Strategic Issues Committee |

Board Credit Committee |

|||||||

Name of Director |

Status |

DOA |

Status |

DOA |

Status |

DOA |

Status |

DOA |

Status |

DOA |

Status |

DOA |

Status |

DOA |

Mr. A W Atukorala |

C |

06.09.2016 |

C |

06.09.2016 |

C |

06.09.2016 |

M |

01.06.2017 |

||||||

Mr. A K Pathirage |

M |

01.01.2014 |

M |

11.08.2011 |

M |

18.02.2011 |

M |

01.06.2017 |

||||||

Mr. P L D N Seneviratne |

M |

01.01.2017 |

M |

01.06.2017 |

||||||||||

Mr. T L F Jayasekara |

M |

10.02.2010 |

M |

10.02.2010 |

C |

10.02.2010 |

M |

19.12.2014 |

M |

11.08.2011 |

||||

Mr. D S P Wikramanayake |

C |

22.06.2010 |

M |

22.06.2010 |

M |

19.12.2014 |

M |

22.06.2010 |

||||||

Mrs. Kimarli Fernando |

M |

22.06.2010 |

M |

30.03.2015 |

M |

11.08.2011 |

M |

19.12.2014 |

M |

04.06.2010 |

C |

01.06.2017 |

||

Mrs. Indrani Sugathadasa |

C |

01.01.2014 |

M |

01.01.2014 |

M |

19.12.2014 |

M |

01.06.2017 |

||||||

Mrs. D M A Harasgama* |

M |

22.04.2015 |

M |

22.04.2015 |

M |

22.04.2015 |

M |

01.06.2017 |

||||||

Mr. D M R Phillips** |

M |

01.01.2017 |

M |

01.06.2017 |

M |

01.06.2017 |

||||||||

Mr. K D W Ratnayaka |

M |

15.03.2016 |

M |

13.05.2015 |

||||||||||

Mr. N S Welikala*** |

M |

11.11.2016 |

M |

11.11.2016 |

M |

11.11.2016 |

M |

11.11.2016 |

||||||

Mr. R Semasinghe**** |

M |

01.12.2017 |

M |

01.12.2017 |

M |

01.12.2017 |

||||||||

DOA - Date of Appointment Status - C - Chairman / M - Member

NUMBER OF MEETINGS HELD AND ATTENDANCE OF THE BOARD SUBCOMMITTEES AS AT 31 DECEMBER 2017

Name of Committee |

Human Resources and Remuneration Committee |

Integrated Risk Management Committee |

Nominations Committee |

Board Audit Committee |

Related Party Transactions Review Committee |

Strategic Issues Committee |

Board Credit Committee |

|||||||

Name of Director |

Eligible to Attend |

Attended |

Eligible to Attend |

Attended |

Eligible to Attend |

Attended |

Eligible to Attend |

Attended |

Eligible to Attend |

Attended |

Eligible to Attend |

Attended |

Eligible to Attend |

Attended |

Mr A W Atukorala |

7 |

7 |

4 |

4 |

3 |

3 |

5 |

5 |

||||||

Mr. A K Pathirage |

4 |

4 |

7 |

7 |

3 |

0 |

5 |

3 |

||||||

Mr. P L D N Seneviratne |

6 |

6 |

5 |

5 |

||||||||||

Mr. T L F Jayasekara |

4 |

4 |

7 |

7 |

7 |

7 |

4 |

3 |

3 |

3 |

||||

Mr. D S P Wikramanayake |

6 |

6 |

7 |

7 |

4 |

4 |

3 |

2 |

||||||

Mrs. Kimarli Fernando |

4 |

4 |

7 |

7 |

7 |

6 |

4 |

4 |

3 |

3 |

5 |

5 |

||

Mrs. Indrani Sugathadasa |

4 |

4 |

7 |

6 |

4 |

4 |

5 |

5 |

||||||

Mrs. D M A Harasgama* |

4 |

4 |

4 |

1 |

2 |

2 |

1 |

1 |

||||||

Mr. D M R Phillips** |

4 |

4 |

3 |

3 |

5 |

3 |

||||||||

Mr. K D W Ratnayaka |

4 |

4 |

6 |

6 |

||||||||||

Mr. N S Welikala*** |

2 |

2 |

2 |

1 |

1 |

1 |

2 |

2 |

||||||

Mr. R Semasinghe**** |

- |

- |

- |

- |

- |

- |

||||||||

* Mrs. D M A Harasgama (Resigned w.e.f 30th June 2017)

** Mr. D M R Phillips (Reappointed to Integrated Risk Management Committee w.e.f 01st June 2017)

*** Mr. N S Welikala (Resigned w.e.f. 30th April 2017)

**** Mr. R Semasinghe (Appointed to Board Audit Committee, Related Party Transactions Review Committee and Integrated Risk Management Committee w.e.f 01st December 2017)

BOARD PERFORMANCE AND EVALUATION

The annual self-evaluation process is used to determine weaknesses in the Board’s own governance practices. The Board annually assesses the effectiveness of the directors’ own governance practices by way of a self-assessment to be undertaken by each director, and maintains records of such assessments.

The Chairman and Deputy Chairman reviews the responses of the directors to the self assessment questionnaire and reports to the Board any identified weaknesses and lapses and where necessary recommends, an action plan for approval to the Board. The Board periodically reviews the progress made on the action plan (if any).

DIRECTORS' REMUNERATION AND DIRECTORS' INTEREST IN SHARES

Please refer the Directors Report on pages 257 and 263 for information on Directors' Remuneration and Directors' Interest in Shares.

CREATING THE RIGHT CULTURE AND VALUES

In 2017, under the Transformation 2020 program, we launched a series of organizational change management and outreach workshops across all regions and Senior Management of the Bank met and engaged every member of the NDB Family to share the Bank’s vision, strategy and values. We believe that to embed cultural change we have to change how our people behave, including challenging established mindsets and attitudes. We launched the OneNDB initiative through which we hope to create a dynamic work culture by integrating the 4 C’s of Communication, Collaboration, Critical thinking and Creativity and strengthening the fabric of trust and commitment within the NDB Family.

Our Five Values : Integrity, Excellence, Creativity, Accountability and Sincerity and our governance related policies are our essential guiding

principle that would cut across the way we do business, all our business transactions, products and services, notably in situations where the rule

book provides no answers.

NDB’s culture and values are driven through the following governance related policies: |

• The Compliance Policy and Code of Conduct themed “Living our Values” constitutes a reference point covering all aspects of employees’ working relationships, specifically (but not exclusively) with other NDB employees, customers, regulators, service providers, suppliers, competitors and the broader community. It also covers the standards of personal integrity that employees of NDB Group are required to exercise in conducting their own private and financial affairs. The Code is a referral point for all governance related policies of the Bank. |

• The Group Securities Trading Policy restricts directors, and employees from trading in NDB securities during certain specified blackout periods. The Policy also prohibits speculative trading in NDB Securities and to support compliance with this requirement a minimum hold requirement was introduced. All employee trades are monitored by the Compliance Department to ensure compliance with this policy. |

• The Group Anti-Bribery & Corruption Policy sets out minimum standards and describes NDB Group’s stance on bribery and corruption. It complements NDB Group’s core values of integrity and the standard of behavior expected from all directors and employees of NDB Group. The Gifts and Entertainment Policy of the Group also forms part of this Policy. |

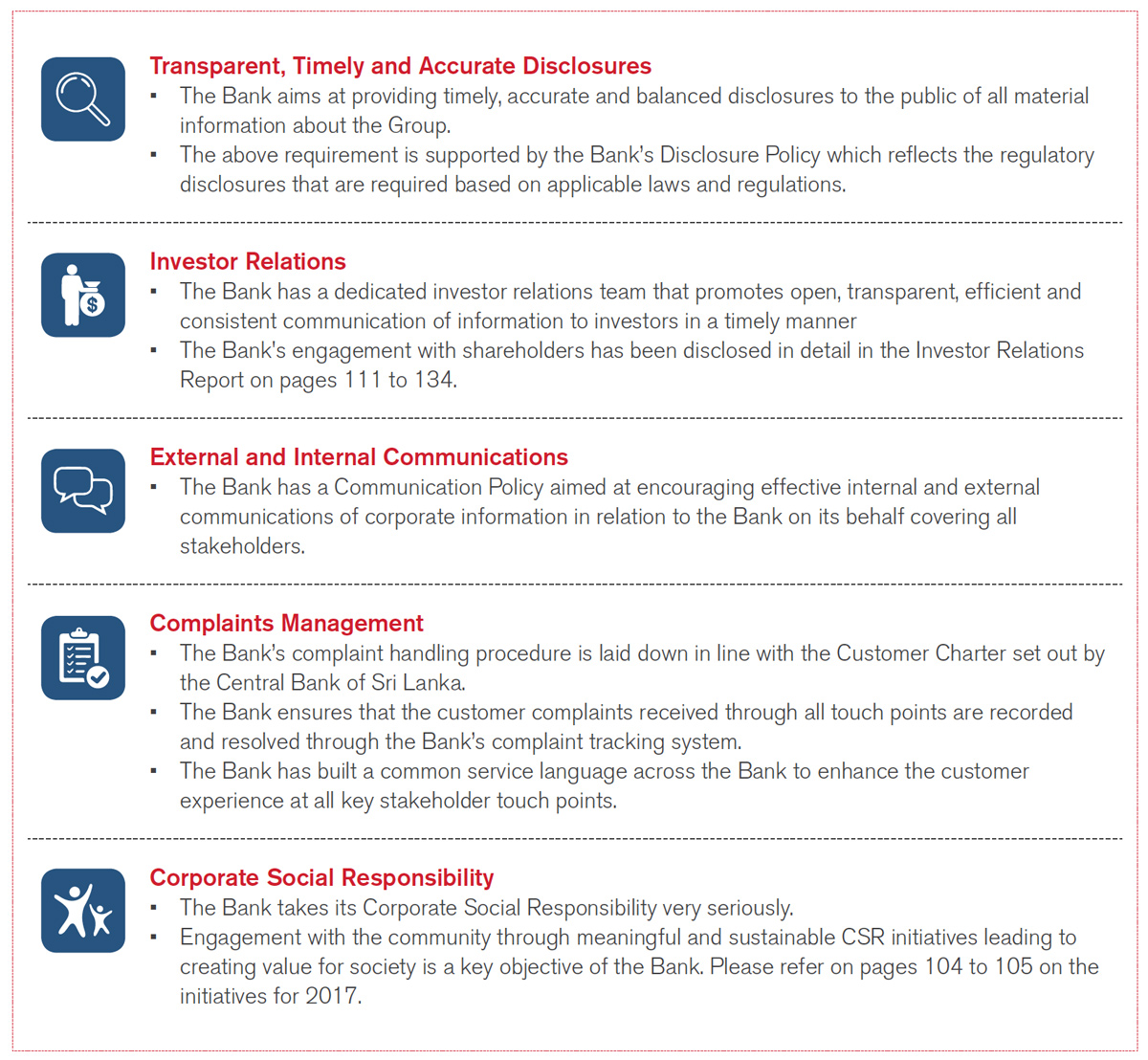

• The Related Party Transactions Policy of the Group lays done the process to identify, approve, monitor and disclose all related party transactions of the Bank. The Bank takes every endeavour to ensure that it does not grant more favorable treatment when entering into a transaction with a related party of the Bank. The Board appointed Related Party Transactions Review Committee in line with the Related Party Policy assesses and considers transactions with related parties of the Bank in order to ensure that related parties are treated on par with other shareholders and constituents of the Bank. The Policy incorporates legal and regulatory requirements on related party transactions. |

• The Whistleblowing Policy of the Bank provides clear procedures for the escalation of complaints and notification of incidents to management and the Board. The Bank encourages employees to report alleged acts of malpractice or misconduct and ensures that all allegations are considered for investigation and suitable action taken where necessary. The whistle-blowing employee is protected against adverse action (discharge, demotion, suspension, harassment, or other forms of discrimination) for raising allegations of misconduct or malpractice. The policy lists down the contact details of the officials of the Bank that employees could escalate their concerns to. |

EFFECTIVE RISK MANAGEMENT AND CONTROL

Our internal controls cover financial, operational, compliance, technology controls, as well as risk management policies and systems.

RISK GOVERNANCE

Maintaining an active focus on risk and compliance underpins how we run our business. We identify and actively manage risks as part of a Group-wide “Risk Management Framework” for which the Board is ultimately responsible. The Integrated Risk Management Committee of the Board supports the Board to carry out certain responsibilities within the risk governance framework.

Risk accountability across the three lines of defense are as detailed on page 142 of this report.

For more on our risk governance framework see the Risk Management Report on page 135 to 186.

STRONG COMPLIANCE CULTURE

Our compliance culture is anchored on transparency, awareness and an emphasis on respecting both the letter and spirit of the law.

We ensure that regulations are disseminated in a timely manner to relevant stakeholders, employees are trained and aware of the changing regulatory environment and applicable laws and regulations are integrated with the Bank’s processes and procedures.

In order to protect its reputation as a responsible corporate citizen, and to meet its legal, regulatory and social obligations, the Bank believes that it is essential to minimizes the risk of its services and operations being used by terrorists, money launderers or other criminals. The Bank has in place a robust Anti Money Laundering Program and framework to support this requirement.

We work closely with our regulators to ensure that our internal governance standards meet their increasing expectations and have frequent interactions with them allowing us to hear any supervisory concerns they may have whilst at the same time keeping them updated on the Bank's key strategies.

IT GOVERNANCE

IT Governance forms an essential part of the Bank’s Governance framework. Alignment to business objectives, prudent expenditure, compliance, risk management, security, and responsible allocation of resources are core principles of NDB’s IT Governance.

The Bank has in place an IT Steering Committee constituted of senior members of the management team representing areas such as Risk, Internal Audit, Operations, IT and Business. In order to ensure business objectives are achieved in a timely manner the IT Steering Committee leverages the experience, expertise and knowledge of individuals within the committee. The committee leads and facilitates roll-out, uptake and on-boarding of IT platforms and technology enabled products and services, resource allocation, monitors the progress and intervene where required to ensure project scope, cost and time objectives are met.

Further, the Risk Department independently assesses technology risk on an ongoing basis. Periodic internal and external audits ensure regular verification of the degree of compliance to policies, procedures, and standards.

The IT Governance disciplines at NDB ensure technology investments made by the Bank are appropriate, and result in customer convenience, competitive advantage, and business growth.

The Bank’s Information Security conforms to the Baseline Security Standard of the Central Bank of Sri Lanka.

GOVERNANCE IN OUR SUBSIDIARIES

The governance framework in our Subsidiaries has been aligned to the governance framework of the Bank in order to achieve consistent standards across the Group. Corporate Governance developments in the subsidiaries of the Bank are monitored regularly in order to ensure that legal and regulatory requirements are up to date. The Bank works closely with its group companies in order to entrench and improve their corporate governance framework.

REGULAR ENGAGEMENT WITH STAKEHOLDERS

The Bank values open and transparent communication with our stakeholders, including shareholders. The Bank regularly communicates information in a range of ways including:

-

Publication of financial reports, announcements, circulars and press releases

-

The Bank's website which includes a dedicated investor relations helpline

-

Shareholder meetings

-

Investor relations communication

-

Quarterly investor forums

-

Teleconferences and webcasts for analysts and media briefings

Channels used by the Bank to strengthen its communication with stakeholders are as follows:

Statement of Compliance - Direction No. 11 of 2007 (as amended) on Corporate Governance issued by the Monetary Board of the Central Bank of Sri Lanka (the Corporate Governance Direction)

The Corporate Governance Direction provides processes and practices deemed to be the framework that facilitates the conduct of the banking business in a responsible and accountable manner so as to promote the safety and soundness of the Bank, thereby leading to the stability of the overall banking sector. The disclosures below reflect the Bank’s compliance with the Corporate Governance Direction under the following key principles:

The responsibilities of the Board;

The Board’s composition;

Criteria for the assessment of the fitness and propriety of Directors;

Management functions delegated by the Board;

The Chairman and Chief Executive Officer;

Board appointed subcommittees;

Related Party Transactions; and

Disclosures;

Rule No. |

Corporate Governance Principles |

Compliance Status |

|||||||||||||||

3 (1) |

Responsibilities of the Board |

||||||||||||||||

3 (1) (i) |

The Board shall strengthen the safety and soundness of the Bank by ensuring the implementation of the following: |

||||||||||||||||

(a) Approve and oversee the bank’s strategic objectives and corporate values and ensure that these are communicated throughout the bank; |

Complied. The Bank’s strategic plan for 2017 - 2020 which launched the Transformation 2020 Program was formally approved by the Board in June 2017. In 2017, the Chief Executive Officer (CEO) and the Senior Management Team personally met with each member of the NDB Team to ensure that the Bank’s new strategic objectives, values and culture was known and understood by all of them. A website dedicated to share progress made on achieving the objectives set out in the Bank’s strategic plan in a clear, transparent and timely manner was also launched in September 2017. |

||||||||||||||||

(b) Approve the overall business strategy of the bank, including the overall risk policy and risk management procedures and mechanisms with measurable goals, for at least the next three years; |

Complied. The Bank’s overall business strategy for 2017-2020 was approved by the Board in June 2017 after detailed discussions held with the Leadership Team of the Bank. The Bank has established an Integrated Risk Management Framework approved by the Board covering all risks. There are separate risk policies and risk management procedures with regard to credit, operational and market risk segments. The Bank has established an Integrated Risk Management Framework covering all risks approved by the Board. This has been further reviewed by the Integrated Risk Management Committee (IRMC) during the year 2017 to ensure that the risk management of the Bank is at acceptable levels. The Bank has a Board approved Strategic Plan for the next 3 years (until 2020) with measurable Key Performance Indicators. |

||||||||||||||||

(c) Identify the principal risks and ensure implementation of appropriate systems to manage the risks prudently; |

Complied. The Board is responsible for the overall risk framework of the Bank. The IRMC appointed by the Board, reviews and recommends to the Board, the Bank’s risk policies and procedures defining the Bank’s risk appetite, identifying principal risks, setting governance structures and implementing policies and systems in line with the Integrated Risk Management Framework to measure, monitor and manage the principal risks of the Bank. The Board has approved risk management policies and procedures as reviewed and recommended by the IRMC, based on these parameters and as required by this Direction. The following reports provide further insight in this regard: • Risk Management Report on pages 135 to 186 • The Board Integrated Risk Management Committee Report on pages 273 to 274. |

||||||||||||||||

(d) Approve implementation of a policy of communication with all stakeholders, including depositors, creditors, shareholders and borrowers; |

Complied. The Bank has in place a Board approved Communication Policy aimed to encourage effective communication of corporate information relating to the Bank on its behalf covering all stakeholders including employees, customers, creditors, shareholders, general public and the regulators. This policy is reviewed annually in order to reflect the best practices in communications. |

||||||||||||||||

(e) Review the adequacy and the integrity of the bank’s internal control systems and management information systems; |

Complied. The Board is assisted by the Board Audit Committee (BAC), who evaluates the adequacy and effectiveness of the internal control systems, and reviews internal control issues identified by the Bank's Group Audit, External Auditor, regulatory authorities and the Management. The Bank has in place a Management Information Systems (MIS) Policy, approved by the Board. The MIS process of the Bank is reviewed by the Bank's Group Audit and was discussed with the BAC. The Board also reviews the adequacy of the Bank’s Management Information Systems, based on the monthly MIS pack submitted to the Board each month. |

||||||||||||||||

(f) Identify and designate key management personnel, as defined in Banking Act Determination No.3 of 2010 on the Assessment of fitness and propriety of officers performing executive functions in LCBs |

Complied. Key Management Personnel (KMPs) of the Bank have been identified by the Board having considered the Banking Act Determination No 3 of 2010 on officers performing executive functions of the Bank, and presently include the following: 1. The Leadership Team whose names are detailed on pages 198 to 201 of this Report; and 2. Chandana Guniyangoda in view of the fact that he holds a directorship in one of the Bank’s subsidiaries. |

||||||||||||||||

(g) Define the areas of authority and key responsibilities for the Board Directors themselves and for the Key Management Personnel; |

Complied. There is a clear division of authority and responsibilities between the directors and the KMPs which is set out in the Bank’s internal Code of Corporate Governance. The directors were set goals and targets for the year 2017. The duties and responsibilities of KMPs are documented in their respective job descriptions. The Board evaluated the performance review objectives of the KMPs . |

||||||||||||||||

(h) Ensure that there is appropriate oversight of the affairs of the bank by key management personnel, that is consistent with board policy; |

Complied. The Board regularly interacts with the Bank’s KMPs through reports tabled at both Board and subcommittee meetings. KMPs make presentations to the Board on matters under their purview and are also called in by the Board to explain matters relating to their areas. Banking operations carried out in line with the Banks’ strategic objectives including any issues faced by the Bank are discussed on an ongoing basis at Board meetings. The CEO at weekly meetings held with The Leadership Team updates them on key decision points taken by the Board. |

||||||||||||||||

(i) Periodically assess the effectiveness of the board directors’ own governance practices, including: (i) the selection, nomination and election of directors and key management personnel; (ii) the management of conflicts of interests; and (iii) the determination of weaknesses and implementation of changes where necessary; |

Complied. The Nominations Committee (NC) has been delegated the function of selection, nomination and election of directors and KMPs to the Board. The Bank and director’s interests are disclosed to the Board and directors who have a particular interest have abstained from voting in such a situation and he/she is not counted in the quorum. Determination of weaknesses in the Board of Directors own governance practices and implementation of changes are addressed through the annual self-evaluation process among the Board members. Self-evaluations for the year 2017 have been collected and summarized by the Company Secretary and submitted to the Chairman & Deputy Chairman for their review .The Chairman then discusses areas of weaknesses and recommend changes where necessary at a Board meeting. |

||||||||||||||||

(j) Ensure that the bank has an appropriate succession plan for key management personnel; |

Complied. The Succession Plan of the Bank was approved by the Board at its meeting held in September 2017. |

||||||||||||||||

(k) Meet regularly, on a needs basis, with the key management personnel to review policies, establish communication lines and monitor progress towards corporate objectives |

Complied. The KMPs are regularly present or are called in for discussions at the meetings of the Board and its subcommittees on policy and other matters relating to their areas. Progress made towards corporate objectives is a regular agenda item for the Board and KMPs are regularly involved in Board level discussions on same. |

||||||||||||||||

(l) Understand the regulatory environment and ensure that the bank maintains an effective relationship with regulators; |

Complied. Circulars, directions and guidelines issued by the regulators are circulated to the directors on a quarterly basis for their information. In 2017 all new laws and regulations that were issued and relevant to banking business were made available on the BoardPac together with an explanatory note which detailed the key areas of impact. The CEO meets with Central Bank officials at the monthly CEO’s meeting. The Chairman of the Bank and the Chairpersons of the Board subcommittees also meet with the CBSL officials. Further directors, the CEO and KMPs of the Bank maintains dialog with the regulators on an ongoing basis. |

||||||||||||||||

(m) Exercise due diligence in the hiring and oversight of external auditors. |

Complied. The Board Audit Committee Charter includes the functions of hiring and overseeing of External Auditors. The BAC carries out the necessary due diligence regarding the hiring/evaluation of the External Auditor and makes recommendations to the Board. The appointment/re-appointment of the External Auditor is made at the Annual General Meeting. Oversight of the External Auditor is carried out by the BAC and the Board is briefed of any concerns in this regard (if required). A formal evaluation of the External Auditors’ performance is completed annually by the BAC and conclusions together with any recommendations are discussed at Board level. |

||||||||||||||||

3(1) (ii) |

The board shall appoint the chairman and the chief executive officer and define and approve the functions and responsibilities of the chairman and the chief executive officer in line with Direction 3(5) of these Directions. |

Complied. The Board has appointed the Chairman and CEO and has approved their functions. There is a clear division of responsibilities between the Chairman and the CEO. Functions and responsibilities of the Chairman and the CEO are documented in the Board approved internal Code of Corporate Governance and is in line with this Direction. |

|||||||||||||||

3(1) (iii) |

The board shall meet regularly and board meetings shall be held at least twelve times a year at approximately monthly intervals. Such regular board meetings shall normally involve active participation in person of a majority of directors entitled to be present. Obtaining the board’s consent through the circulation of written resolutions/papers shall be avoided as far as possible. |

Complied. Regular monthly Board meetings are held and special Board meetings are scheduled as and when the need arises. There have been 14 Board meetings during 2017 which included 2 special meetings. In addition, the subcommittees of the Board meet as and when necessary. 5 Circular resolutions have been passed during 2017. Circulation of Board papers to obtain Board’s consent is minimized and resorted to only when absolutely necessary. These decisions are in any event later confirmed/ratified by the Board at the immediately succeeding Board meeting. |

|||||||||||||||

3(1) (iv) |

The board shall ensure that arrangements are in place to enable all directors to include matters and proposals in the agenda for regular board meetings where such matters and proposals relate to the promotion of business and the management of risks of the bank. |

Complied. All directors are entitled to include matters and proposals in the agenda for Board meetings and this right has been entrenched in the Bank’s internal Code of Corporate Governance. Monthly meetings are scheduled and informed to the Board at the beginning of each calendar year to enable submission of proposals in the agenda for regular meetings. This process supports the requirement detailed in this Direction and a director may include a proposal (if required) in the agenda of a Board meeting. |

|||||||||||||||

3(1) (v) |

The board procedures shall ensure that notice of at least 7 days is given of a regular board meeting to provide all directors an opportunity to attend. For all other board meetings, reasonable notice may be given. |

Complied. Monthly meetings are scheduled and informed to the Board at the beginning of each calendar year to provide directors an opportunity to attend. Formal notice of meetings, the agenda and Board papers related to each Board meeting are circulated at least 7 days in advance of the Board meeting. These documents are uploaded through a secure connection to the tablets of all directors. |

|||||||||||||||

3(1) (vi) |

The board procedures shall ensure that a director who has not attended at least two-thirds of the meetings in the period of 12 months immediately preceding or has not attended the immediately preceding three consecutive meetings held, shall cease to be a director. Participation at the directors’ meetings through an alternate director shall, however, be acceptable as attendance. |

Complied. The Company Secretary monitors the attendance register to ensure compliance. All directors have attended at least two thirds of the meetings held during the years 2017 and no director has been absent from three consecutive meetings during 2017. Attendance of Directors at Board meetings is detailed on page 213. |

|||||||||||||||

3(1) (vii) |

The board shall appoint a company secretary who satisfies the provisions of Section 43 of the Banking Act No. 30 of 1988, whose primary responsibilities shall be to handle the secretariat services to the board and shareholder meetings and to carry out other functions specified in the statutes and other regulations. |

Complied. Company secretary appointed by the Board is an Attorney at Law who satisfies the provision of Section 43 of the Banking Act. The internal Code of Corporate Governance includes the responsibilities of the Company Secretary as specified in the statutes and other regulations. |

|||||||||||||||

3(1) (viii) |

All directors shall have access to advice and services of the company secretary with a view to ensuring that board procedures and all applicable rules and regulations are followed. |

Complied. The internal Code of Corporate Governance of the Bank includes a provision to enable all directors to have access to the advice and services of the Company Secretary. For the year 2017, the Company Secretary has provided assistance to the directors when requested. |

|||||||||||||||

3(1) (ix) |

The company secretary shall maintain the minutes of board meetings and such minutes shall be open for inspection at any reasonable time, on reasonable notice by any director. |

Complied. The Company Secretary maintains detailed Board minutes and circulates minutes to all directors. The minutes are approved at the subsequent Board meetings. The Bank’s internal Code of Corporate Governance also provides that minutes are open for inspection at any reasonable time, upon reasonable notice given by any director. Additionally, copies have been provided of previous meetings to directors when requested. |

|||||||||||||||

3(1) (x) |

Minutes of board meetings shall be recorded in sufficient detail so that it is possible to gather from the minutes, as to whether the board acted with due care and prudence in performing its duties. The minutes shall also serve as a reference for regulatory and supervisory authorities to assess the depth of deliberations at the board meetings. Therefore, the minutes of a board meeting shall clearly contain or refer to the following: (a) a summary of data and information used by the board in its deliberations; (b) the matters considered by the board; (c) the fact-finding discussions and the issues of contention or dissent which may illustrate whether the board was carrying out its duties with due care and prudence; (d) the testimonies and confirmations of relevant executives which indicate compliance with the board’s strategies and policies and adherence to relevant laws and regulations; (e) the board’s knowledge and understanding of the risks to which the bank is exposed and an overview of the risk management measures adopted; and (f) the decisions and board resolutions. |

Complied. A Board approved procedure is in place for recording the Board minutes by the Company Secretary. The minutes contain adequate details appropriate to the matters dealt with. The minutes are read together with the corresponding Board papers, which supplement information in the minutes. All matters required to be minuted in terms 3(1) (x ) (a) – (f) are recorded in the minutes. |

|||||||||||||||

3(1) (xi) |

There shall be a procedure agreed by the board to enable directors, upon reasonable request, to seek independent professional advice in appropriate circumstances, at the bank’s expense. The board shall resolve to provide separate independent professional advice to directors to assist the relevant director or directors to discharge his/her/their duties to the bank. |

Complied. As per the Bank’s internal Code of Corporate Governance there is a process for Board members to obtain Independent professional advice at the expense of the Bank. The Board has obtained professional advice during the year. |

|||||||||||||||

3(1) (xii) |

Directors shall avoid conflicts of interests, or the appearance of conflicts of interest, in their activities with, and commitments to, other organizations or related parties. If a director has a conflict of interest in a matter to be considered by the board, which the board has determined to be material, the matter should be dealt with at a board meeting, where independent non-executive directors [refer to Direction 3(2)(iv) of these Directions] who have no material interest in the transaction, are present. Further, a director shall abstain from voting on any board resolution in relation to which he/she or any of his/her close relation or a concern in which a director has substantial interest, is interested and he/she shall not be counted in the quorum for the relevant agenda item at the board meeting. |

Complied. The directors are conscious of their obligations to deal with situations where there is a conflict of interest in accordance with the Articles of Association of the Bank and the Corporate Governance Direction No 11 of 2007 (as amended) The internal Code of Corporate Governance adopted by the Board, requires each Board member to determine whether he/ she has a potential or actual conflict of interest. If a director of the Bank has a conflict of interest in a matter to be considered by the Board, which the Board has determined to be material, such matters are disclosed and discussed at the Board meetings, where independent Non Executive directors who have no material interest in the transaction, are present. Further directors abstain from voting on Board resolutions in relation to which such directors or any of their close relation/s or a concern in which such directors have substantial interest, and/or are interested in. Further their votes are not counted in the quorum for the relevant agenda item at the Board meeting. |

|||||||||||||||

3(1) (xiii) |

The board shall have a formal schedule of matters specifically reserved to it for decision to ensure that the direction and control of the bank is firmly under it's authority. |

Complied. Board has a formal schedule of matters specifically reserved to it for decision to ensure that direction and control of the Bank is firmly under its authority. |

|||||||||||||||

3(1) (xiv) |

The board shall, if it considers that the bank is, or is likely to be, unable to meet its obligations or is about to become insolvent or is about to suspend payments due to depositors and other creditors, forthwith inform the director of Bank Supervision of the situation of the bank prior to taking any decision or action. |

Complied. The Bank is aware of the requirement but the situation has not arisen within the year. A Solvency Statement is prepared quarterly and tabled at the IRMC and the Board. The Bank also has an IRMC approved Liquidity Contingency Funding Plan in place. |

|||||||||||||||

3(1) (xv) |

The board shall ensure that the bank is capitalized at levels as required by the Monetary Board in terms of the capital adequacy ratio and other prudential grounds. |

Complied. Monthly and quarterly compliance reports have been submitted to the Board which contains the Capital Adequacy Ratio (CAR). The Bank is fully compliant with the Capital Adequacy requirements stipulated by the Central Bank of Sri Lanka. Also the ICAAP covers capital planning over the next 3 years. |

|||||||||||||||

3(1) (xvi) |

The board shall publish in the bank’s Annual Report, an annual corporate governance report setting out the compliance with Direction 3 of these Directions. |

Complied. This requirement is met through the presentation of this Report. |

|||||||||||||||

3(1) (xvii) |

The board shall adopt a scheme of self-assessment to be undertaken by each director annually, and maintain records of such assessments. |

Complied. The Board has a scheme of annual self-assessment and records are maintained by the Company Secretary. |

|||||||||||||||

3(2) |

The Board’s Composition |

||||||||||||||||

3(2) (i) |

The number of directors on the board shall not be less than 7 and not more than 13. |

Complied. The number of Board directors during the year 2017 was in compliance with the thresholds detailed in this direction. As at 31st December 2017, the Board comprised of ten (10) directors. |

|||||||||||||||

3(2) (ii) |

The total period of service of a director other than a director who holds the position of chief executive officer shall not exceed nine years. |

Complied. None of the directors have exceeded 9 years of service during the year 2017.The Company Secretary monitors this requirement. |

|||||||||||||||

3(2) (iii) |

An employee of a bank may be appointed, elected or nominated as a director of the bank (hereinafter referred to as an “executive director”) provided that the number of executive directors shall not exceed one-third of the number of directors of the board. In such an event, one of the executive directors shall be the chief executive officer of the bank. |

Complied. The CEO of the Bank is the only executive director and thus the Bank complies with this requirement. |

|||||||||||||||

3(2) (iv) |

The board shall have at least three independent non-executive directors or one third of the total number of directors, whichever is higher. A non-executive director shall not be considered independent if he/she: a) has direct and indirect shareholdings of more than 1 per cent of the bank; b) currently has or had during the period of two years immediately preceding his/her appointment as director, any business transactions with the bank as described in Direction 3(7) hereof, exceeding 10 per cent of the regulatory capital of the bank. c) has been employed by the bank during the two year period immediately preceding the appointment as director; d) has a close relation who is a director or chief executive officer or a member of key management personnel or a material shareholder of the bank or another bank. For this purpose, a “close relation” shall mean the spouse or a financially dependent child; e) represents a specific stakeholder of the bank; f) is an employee or a director or a material shareholder in a company or business organization: I. which currently has a transaction with the bank as defined in Direction 3(7) of these Directions, exceeding 10 per cent of the regulatory capital of the bank, or II. in which any of the other directors of the bank are employed or are directors or are material shareholders; or III. in which any of the other directors of the bank have a transaction as defined in Direction 3(7) of these Directions, exceeding 10 per cent of regulatory capital in the bank; |

Complied. The Board assesses the independence or non-independence of each non-executive director based on a declaration made by each director to the Company Secretary each year. During 2017, the number of independent non-executive directors exceeded one - third of the total number of directors on the Board. As at 31st December 2017 there were 6 independent non-executive directors on the Board. The non-executive directors are detailed on page 212 of this report. |

|||||||||||||||

3(2) (v) |

In the event an alternate director is appointed to represent an independent director, the person so appointed shall also meet the criteria that applies to the independent director. |

Complied. Directors appoint alternate directors in line with the Articles of the Bank as and when required for a particular meeting. During the year 2017, alternate directors appointed for a particular meeting met the criteria that applies to an independent director. |

|||||||||||||||

3(2) (vi) |

Non-executive directors shall be persons with credible track records and/or have necessary skills and experience to bring an independent judgment to bear on issues of strategy, performance and resources. |

Complied. A Board approved procedure to select and appoint Non Executive directors is in place. The non-executive directors of the Bank are persons with credible track records and have necessary skills and experience to bring an independent judgment to bear on issues of strategy, performance, risks and resources. Please refer the profiles of non-executive directors on pages 188 to 197 of this Report. |

|||||||||||||||

3(2) (vii) |

A meeting of the board shall not be duly constituted, although the number of directors required to constitute the quorum at such meeting is present, unless more than one half of the number of directors present at such meeting are non-executive directors. |

Complied. The attendance of directors is monitored by the Company Secretary. All Board meetings have met this requirement as 90% of the Board comprises of non-executive directors. |

|||||||||||||||

3(2) (viii) |

The independent non-executive Directors shall be expressly identified as such in all corporate communications that disclose the names of Directors of the bank. The bank shall disclose the composition of the board, by category of Directors, including the names of the chairman, executive Directors, non-executive Directors and independent non-executive Directors in the annual corporate governance report. |

Complied. The Independent non-executive directors are expressly identified as such in all corporate communications that disclose the names of directors of the Bank. The composition of the Board, by category of directors, including the names of the Chairman, executive director, non-executive directors and independent non-executive directors are given on pages 212 to 213 of this Report. |

|||||||||||||||

3(2) (ix) |

There shall be a formal, considered and transparent procedure for the appointment of new directors to the board. There shall also be procedures in place for the orderly succession of appointments to the board. |

Complied. There is in place a formal, considered and transparent procedure for the appointment of new directors to the Board. In practice, directors are appointed based on recommendations made by the NC. |

|||||||||||||||

3(2) (x) |

All directors appointed to fill a casual vacancy shall be subject to election by shareholders at the first general meeting after their appointment. |

Complied. Appointment to fill a casual vacancy is made by the Board on the recommendations of the NC. A person so appointed would stand for re-election at the next Annual General Meeting in accordance with the Articles of Association. No directors were appointed in 2017 to fill causal vacancies. |

|||||||||||||||

3(2) (xi) |

(a) If a director resigns or is removed from office, the board shall: (a) announce the director’s resignation or removal and the reasons for such removal or resignation including but not limited to information relating to the relevant director’s disagreement with the bank, if any; and (b) issue a statement confirming whether or not there are any matters that need to be brought to the attention of shareholders. |

Complied. Mrs. D M A Harasgama and Mr. N S Welikala resigned from the Bank in 2017. The Bank informed the regulatory authorities and shareholders as per CSE requirements of such resignation stating the reasons for such resignation and confirming that there were no matters that needed to be brought to the attention of shareholders. |

|||||||||||||||

3(2) (xii) |

A director or an employee of a bank shall not be appointed, elected or nominated as a director of another bank except where such bank is a subsidiary company or an associate company of the first mentioned bank. |

Complied. The NC takes into account this requirement in their deliberations when considering the appointments of directors. The Banks “Compliance Policy and Code of Conduct" further incorporates this requirement for Employees. No directors or Employees of the Bank is a director of another Bank. |

|||||||||||||||

3(3) |

CRITERIA TO ASSESS THE FITNESS AND PROPRIETY OF DIRECTORS |

||||||||||||||||

3(3) (i) |

The age of a person who serves as director shall not exceed 70 years. |

Complied. There are no directors who are over 70 years of age. |

|||||||||||||||

3(3) (ii) |

A person shall not hold office as a director of more than 20 companies/entities/institutions inclusive of subsidiaries or associate companies of the bank. |

Complied. No director holds directorships of more than 20 companies. The other directorships of each of the directors is disclosed in pages 190 to 197 of the annual report |

|||||||||||||||

3(3) |

MANAGEMENT FUNCTION DELEGATED BY the BOARD |

||||||||||||||||

3(4) (i) |

The directors shall carefully study and clearly understand the delegation arrangements in place. |

Complied. The Board periodically reviews and approves the delegation arrangements in place to ensure they are relevant and addresses the needs of the Bank. Delegation papers are prepared in detail and recommended by the IRMC to the Board. Terms of Reference (TOR) of each of the Board subcommittees which are incorporated in the respective charters of each Board subcommittee are approved by the Board. In addition it is to be noted that by delegating, the Board does not lose the authority to deal with matters that have been delegated when necessary. |

|||||||||||||||

3(4) (ii) |

The board shall not delegate any matters to a board committee, chief executive officer, executive directors or Key Management Personnel, to an extent that such delegation would significantly hinder or reduce the ability of the board as a whole to discharge its functions. |

||||||||||||||||

3(4) (iii) |

The board shall review the delegation processes in place on a periodic basis to ensure that they remain relevant to the needs of the bank. |

||||||||||||||||

3(5) |

THE CHAIRMAN AND CHIEF EXECUTIVE OFFICER |

||||||||||||||||

3(5) (i) |

The roles of chairman and chief executive officer shall be separate and shall not be performed by the same individual. |

Complied. The roles of Chairman and CEO of the Bank are held by separate individuals. In addition, there is a clear division of responsibilities between the Chairman and the CEO thereby maintaining the balance of power between the two roles. |

|||||||||||||||

3(5) (ii) |

The chairman shall be a non-executive director and preferably an independent director as well. In the case where the chairman is not an independent director, the board shall designate an independent director as the Senior Director with suitably documented terms of reference to ensure a greater independent element. The designation of the Senior Director shall be disclosed in the bank’s Annual Report. |

Complied. The Chairman Mr. A W Atukorala is an independent non-executive director of the Bank. Therefore, the appointment of an independent director as the Senior director does not arise. |

|||||||||||||||

3(5) (iii) |

The board shall disclose in its corporate governance report, which shall be an integral part of its Annual Report, the identity of the chairman and the chief executive officer and the nature of any relationship [including financial, business, family or other material/relevant relationship(s)], if any, between the chairman and the chief executive officer and the relationships among members of the board. |

Complied. The Company Secretary obtains a declarations from each director to identify the nature of any relationship [including financial, business, family or other material/relevant relationship(s)], if any, between the Chairman and the CEO and the relationships among members of the Board in accordance with this direction. Based on the said declarations there are no material relationships between the Chairman and the CEO and among the Board members. |

|||||||||||||||

3(5) (iv) |

The chairman shall: (a) provide leadership to the board; (b) ensure that the board works effectively and discharges its responsibilities; and (c) ensure that all key and appropriate issues are discussed by the board in a timely manner. |

Complied. The Chairman is responsible for the running of the Board, preserving order and ensuring that proceedings at meetings are conducted in a proper manner. Further, he ascertains the views of the directors on the issues being discussed before decisions are taken. The self- evaluation process carried out by the members of the Board each year assists the Chairman to effectively carry out his responsibilities by providing him the required feedback. |

|||||||||||||||

3(5) (v) |

The chairman shall be primarily responsible for drawing up and approving the agenda for each board meeting, taking into account where appropriate, any matters proposed by the other directors for inclusion in the agenda. The chairman may delegate the drawing up of the agenda to the company secretary. |

Complied. The Chairman draws up the agenda in consultation with the CEO and Company Secretary. The Bank’s internal Code of Corporate Governance also casts this responsibility with the Chairman. |

|||||||||||||||

3(5) (vi) |

The chairman shall ensure that all directors are properly briefed on issues arising at board meetings and also ensure that directors receive adequate information in a timely manner. |

Complied. The directors are adequately briefed in the course of discussions by the Chairman, CEO and officers of management in respect of matters that are taken up by the Board. The following procedures are in place to ensure this: • Board papers are circulated in advance among the directors. • Management information is provided on a regular basis to enable directors to assess the performance and stability of the Bank. • Relevant KMPs are on hand for explanations and clarifications. • Directors are able to seek independent professional advice on a needs basis at the Bank’s expense. |

|||||||||||||||

3(5) (vii) |

The chairman shall encourage all directors to make a full and active contribution to the board’s affairs and take the lead to ensure that the board acts in the best interests of the bank. |

Complied. The Chairman ensures that all members effectively participate as a team in Board decisions and directors concerns and comments are duly recorded in the minutes. |

|||||||||||||||

3(5) (viii) |

The chairman shall facilitate the effective contribution of non-executive directors in particular and ensure constructive relations between executive and non-executive directors. |

Complied. All directors of the Board except the CEO are non-executive directors which encourages active participation. Further, non-executive directors participate in Board appointed subcommittees providing further opportunity for active participation. In addition, the feedback received from the self-evaluation process carried out by the Board supports the Chairman in improving contributions of non-executive directors. |

|||||||||||||||

3(5) (ix) |

The chairman, shall not engage in activities involving direct supervision of key management personnel or any other executive duties whatsoever. |

Complied. Chairman is a non-executive director and he does not directly get involved in the supervision of KMPs or any other executive duties. “Role of the Chairman” is included in the Bank’s internal Code of Corporate Governance. |

|||||||||||||||

3(5) (x) |

The chairman shall ensure that appropriate steps are taken to maintain effective communication with shareholders and that the views of shareholders are communicated to the board. |

Complied. Shareholders are encouraged to provide their feedback to the Company Secretary using feedback forms made available with the Annual Report. In addition, there is an e-mail address dedicated for investor relations and the link is available on the Bank’s website. The Bank also has a dedicated Investor Relations Team. The Chairman together with the CEO ensures effective communication with shareholders through investor’s forums held each quarter and through continuous engagements with our institutional investors. Members of the Board are apprised of the views of major investors and other key stakeholders pursuant to these meetings. |

|||||||||||||||

3(5) (xi) |

The chief executive officer shall function as the apex executive-in-charge of the day-to-day-management of the bank’s operations and business. |

Complied. The CEO is responsible for providing the leadership, expertise and professional environment within the Bank for the implementation of the Board’s policies and the achievement of the Bank’s goals and objectives. The operations of the Bank are carried out in conformity to this requirement. |

|||||||||||||||

3(6) |

BOARD APPOINTED COMMITTEES |

||||||||||||||||

3(6) (i) |

Each bank shall have at least four board committees as set out in Directions 3(6)(ii), 3(6)(iii), 3(6)(iv) and 3(6)(v) of these Directions. Each committee shall report directly to the board. All committees shall appoint a secretary to arrange the meetings and maintain minutes, records, etc., under the supervision of the chairman of the committee. The board shall present a report of the performance on each committee, on their duties and roles at the annual general meeting. |

Complied. The Board has established a Strategic Issues Committee, Credit Committee and a Related Party Transactions Review Committee in addition to the four Board subcommittees required in terms of the Direction, namely the Board Audit Committee, Human Resources and Remuneration Committee, Nominations Committee and Integrated Risk Management Committee. The TOR of the Corporate Governance and Legal Affairs Committee was amalgamated and included into the TOR of the IRMC. Recommendations of such committees are addressed directly to the Board and minutes of the same are discussed and noted at the main Board Meeting. This Annual report includes individual reports of each such subcommittee on pages 268 to 280 which reports include a summary of duties, roles and performance of each subcommittee. |

|||||||||||||||

3(6) (ii) |

The following rules shall apply in relation to the Audit Committee: |

||||||||||||||||

(a) The chairman of the committee shall be an independent non-executive director who possesses qualifications and experience in accountancy and/or audit. |

Complied. Mr. T L F Jayasekara, the Chairman of the BAC is an independent non-executive director and a Fellow Member of the Institute of Chartered Accountants of Sri Lanka and an Associate Member of the Chartered Institute of Management Accountants, UK. |

||||||||||||||||

(b) All members of the committee shall be non-executive directors. |

Complied. All members of the BAC are non-executive directors. |

||||||||||||||||

(C) The committee shall make recommendations on matters in connection with: (i) the appointment of the external auditor for audit services to be provided in compliance with the relevant statutes; (ii) the implementation of the Central Bank guidelines issued to auditors from time to time; (iii) the application of the relevant accounting standards; and (iv) the service period, audit fee and any resignation or dismissal of the auditor; provided that the engagement of the Audit partner shall not exceed five years, and that the particular Audit partner is not re-engaged for the audit before the expiry of three years from the date of the completion of the previous term. |

Complied. The matters referred to in the Direction are reviewed and appropriate recommendations are made by the BAC; (i) Re-appointment of the external auditor for audit services has been recommended to the Board by the BAC, after reviewing the performance of the external auditor. The BAC has discussed the audit plan and methodology with the external auditors. (ii) – (iii) BAC has discussed the implementation of the Central Bank guidelines issued to auditors from time to time and the application of the relevant accounting standards; (iv) The external Audit Partner was rotated during 2013 as per the five-year rotation requirement, in order to ensure the independence of the auditor to comply with the requirements of this Direction. The BAC evaluates and makes recommendations to the Board with regard to the audit fee. Refer the ‘Report of the Board Audit Committee’ given on pages 275 to 277. |

||||||||||||||||

(d) The committee shall review and monitor the external auditor’s independence and objectivity and the effectiveness of the audit processes in accordance with applicable standards and best practices. |

Complied. The BAC obtains representations from the external auditor on their independence and that the audit is carried out in accordance with the Sri Lanka Accounting Standards. |

||||||||||||||||

(e) The Committee shall develop and implement a policy on the engagement of an External Auditor to provide non-audit services that are permitted under the relevant statutes, regulations, requirements and guidelines. In doing so, the Committee shall ensure that the provision by an External Auditor of non-audit services does not impair the External Auditor’s independence or objectivity. When assessing the External Auditor’s independence or objectivity in relation to the provision of non-audit services, the Committee shall consider: (i) whether the skills and experience of the audit firm make it a suitable provider of the non-audit services; (ii) whether there are safeguards in place to ensure that there is no threat to the objectivity and/or independence in the conduct of the audit resulting from the provision of such services by the External Auditor; and (iii) whether the nature of the non-audit services, the related fee levels and the fee levels individually and in aggregate relative to the audit firm, pose any threat to the objectivity and/or independence of the External Auditor. |

Complied. A Policy for ‘Engaging the external auditor for non-audit services’ is in place which covers all aspects stated in this Direction. This Policy was reviewed and updated by the BAC and Board in October 2017. |

||||||||||||||||

(f) The Committee shall, before the audit commences, discuss and finalize with the External Auditors the nature and scope of the audit, including: (i) an assessment of the Bank’s compliance with the relevant Directions in relation to corporate governance and the management’s internal controls over financial reporting; (ii) the preparation of Financial Statements for external purposes in accordance with relevant accounting principles and reporting obligations; and (iii) the co-ordination between firms where more than one audit firm is involved. |

Complied. The BAC Charter requires the BAC to discuss and finalize with the external auditor the nature and scope of the audit. In order to comply, the external auditors make a presentation at the BAC meeting detailing the proposed audit plan and scope. The Committee discussed and finalized the audit plan, methodology and scope with the external auditor to ensure that it includes: An assessment of the Bank’s compliance with the relevant Directions in relation to corporate governance and internal controls over financial reporting; The preparation of financial statements for external purposes in accordance with relevant accounting principles and reporting obligations. All audits within the Group other than NDB Capital Bangladesh are carried out by the same external auditor. In respect of NDB Capital Bangladesh, the NDB external auditor coordinates directly and if there are any issues, they are discussed with the BAC. |

||||||||||||||||