RISK MANAGEMENT

The environment, in which the Bank operates in, is changing at a faster rate than usual with changing global geopolitical, economic and technological landscape and is further complicated by ever evolving regulatory environment. This new norm requires banks to enhance risk management capabilities and insights to facilitate more robust and better risk decision making processes, to ensure that the Bank continues to create value to business partners, whilst ensuring resilience to weather the storm of change.

The Bank is currently going through an intense change program known as Transformation 2020 (T20), to become one of the largest banks in Sri Lanka by 2020, increasing balance sheet size and significantly growing stakeholder returns. With evolving business complexity and needs, Group Risk keeps abreast with trends and challenges of risk management to better support the Bank and its Group companies in meeting its strategic and business objectives.

THE RISK PROFILE OF THE BANK AT A GLANCE

Diversified Portfolio

Diversified Portfolio

-

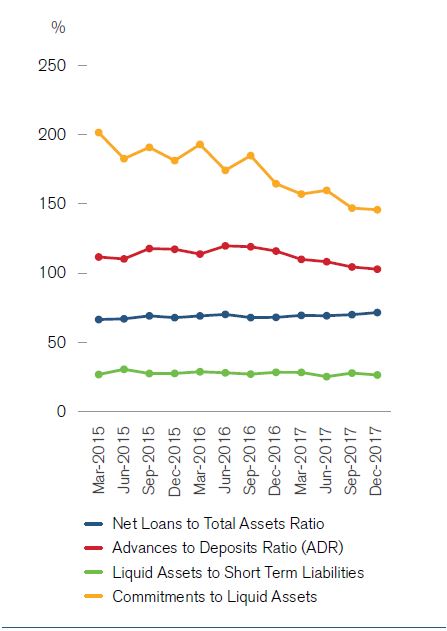

The Bank has a well-diversified portfolio of loans and receivables and income streams across geographies, industry sectors and products.

-

The Bank holds a diverse mix of collateral, valued conservatively.

-

The Bank’s top corporate exposures are stable as a proportion of capital resources and highly diversified.

-

The Bank’s asset quality remains sound.

Prudent Capital & Liquidity Position

Prudent Capital & Liquidity Position

-

The Bank remains adequately capitalized under Basel III requirements and the Bank’s Statement of Financial Position remains liquid.

-

The Bank’s customer deposit base is diversified and is growing.

-

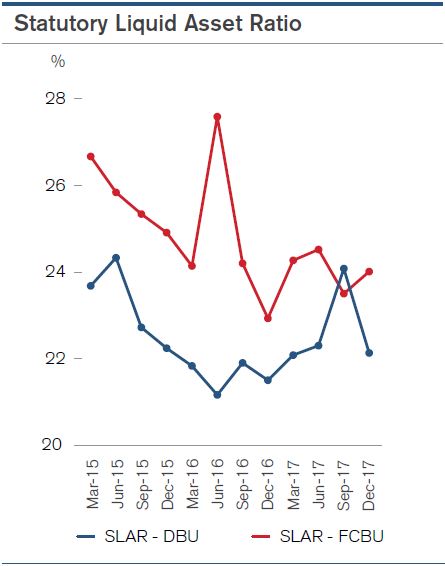

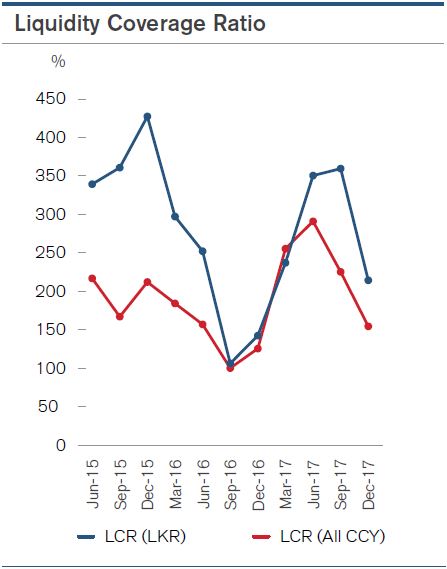

The Bank has a substantial portfolio of high quality liquid assets that can be realized if a liquidity stress occurs which is reflected by maintenance of a Liquidity Coverage Ratio well above the regulatory requirements. The Bank maintains the Liquid Assets Ratio at prudent level.

-

Apart from the regulatory limits, the Bank has set internal prudential Liquidity ratios and Position limits for proactive Liquidity Management.

Robust Risk Governance Structure & Experienced Team

Robust Risk Governance Structure & Experienced Team

-

The Bank has a clear statement of risk appetite which is aligned to the Bank’s strategy and is approved by the Board.

-

The Bank continuously monitors its risk profile to ensure it remains within the risk appetite and regularly conducts stress tests.

-

The Bank reviews and adjusts exposures, underwriting standards and limits in response to observed and anticipated changes in the environment and expectations.

-

The Bank has a very experienced risk team.

-

The Bank has a robust risk management framework which assigns accountability and responsibility for the management and control of risk.

2017 - KEY ACHIEVEMENTS

Establishment of a Board Credit Committee

A Board Credit Committee was formed to further strengthen the credit approval process of the Bank.

Automation of Operational Risk Management Process

Automation facilitates incident/loss event reporting, Risk and Control Self- Assessment (RCSA), Key Risk Indicators (KRIs), Scenario Analysis etc.

Pricing to Reflect Additional Costs of Business

RORAC model revisited in line with increase in Basel III capital requirements.

Risk Models to Support Decision Making

New score card developed statistically based on Bank’s own default experience for Personal Loans to support decision making.

Independent third party validation of risk models carried out based on the Board approved Model Validation Policy.

Basel III Compliance

Group wide risk appetite framework put in place to define the boundaries and drivers of doing business

2018 – OUR PRIORITIES

SLFRS 9 Compliance

Maximize capital utilization

Risk profiling and Scenario based stress testing for Operational Risk

Further strengthening of risk and compliance culture across the Group

Continuing to develop risk talent across the Group Risk Management department

Review and manage Risk Appetite in line with T20 strategy

In the current operating environment, the key to a sustainable business and enduring growth hinges considerably on a bank’s ability to spot and react swiftly to threats and opportunities ahead of other competitors. With this in mind, Group Risk is steadfast in playing a vital role through closer collaboration with business and other functions of the Bank and the Group to meet the shifts in expectations of the myriad of stakeholders (i.e. employees, customers, regulators, shareholders, business partners), while staying vigilant by having the necessary mitigating actions to pro-actively manage risks.

EXTERNAL DRIVERS - IMPACT & RESPONSE

Growth/Performance of World Economy & Local Economy

The Bank monitors these trends carefully to support decision making at operational and strategic levels.

Geo Political Events

The Bank actively monitors situations that could have an impact and conducts regular stress tests of the impact of such events on portfolios.

Monetary Policy, Market Conditions & Economic Climate

Monetary Policy changes and Market conditions will effect the Bank performance. Thus, these are monitored closely to manage risk and exploit opportunities through dynamic Asset and Liability Management.

Changes in Regulatory Environment

The Bank reviews key regulatory developments in order to anticipate changes and their potential impact on performance. The Bank responds both unilaterally and through participation in industry groups to consultation papers and discussions initiated by regulators. The focus of these activities is to develop the framework for a stable and sustainable financial sector and economy. The nature and impact of changes in economic policies, laws and regulations are monitored and considered in the way the Bank conducts business and manages capital and liquidity.

Cyber Threats

The Bank having understood the importance of managing the cyber risk has deployed technical controls to mitigate cyber risk such as multi-layer firewalls, network separation, implementation of intrusion prevention systems, gateway level content filtering, anti-malware solutions and updates to operating systems.

In addition to the above, Bank has subscribed to the services provided by Financial Sector Computer Security Incident Response Team (FINCSIRT), where latest threat intelligence to the Banking industry is provided to IT security team of the Bank to take proactive steps to address the potential exposures. The Bank’s IT policies and procedures are aligned with Baseline Security Standards Guidelines issued by the Central Bank of Sri Lanka. The Bank has also conducted penetration testing exercise by employing an external service provider to test the resilience of systems.

RISK MANAGEMENT APPROACH

The Bank’s risk management is underpinned by a comprehensive, Integrated Risk Management Framework, which is constantly evolving and enhancing to remain relevant and most effective. The framework which is approved by the Board spells out the Bank’s approach to Risk Management. The framework sets out the process of identifying, measuring, monitoring and controlling the different types of risks and the risk governance structure in place. The main objectives of the framework are;

-

To establish common principles, standards for the management and control of all risks and to inform behaviour across the Bank.

-

Provide a shared framework and language to improve awareness of risk management processes among all stakeholders.

-

To provide clear accountability and responsibility for Risk Management.

-

To ensure consistency throughout the Bank in Risk Management.

-

Define the Bank’s risk appetite and align its portfolios and business strategy accordingly.

-

Optimize risk return decisions.

-

Maintain/manage the Bank’s capital adequacy and liquidity position.

-

Further strengthen governance, controls and accountability across the organization.

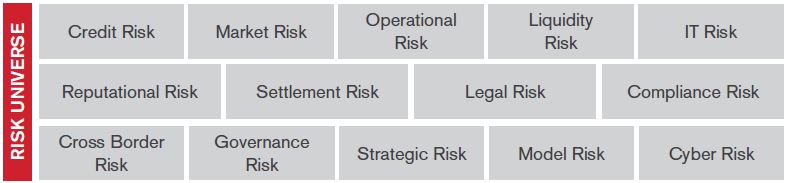

In addition to the main risks (viz. Credit Risk, Market Risk and Operational Risk), the Bank has considered several other risks which are material to it. These additional risk categories include, Liquidity Risk, Interest Rate Risk in the Banking Book, Underestimation of Credit Risk in Standardized Approach, Residual Credit Risk, Concentration Risk, Compliance Risk, Legal Risk, Strategic Risk, Governance Risk, Cross-border Risk, Settlement Risk, Reputational Risk, Model Risk and Group Risk.

The Bank's risk management framework is employed at all levels of the organization, and is instrumental in aligning the behaviour of individuals with the overall attitude to assuming and managing risk and ensuring that Bank’s risk profile is aligned to its risk appetite.

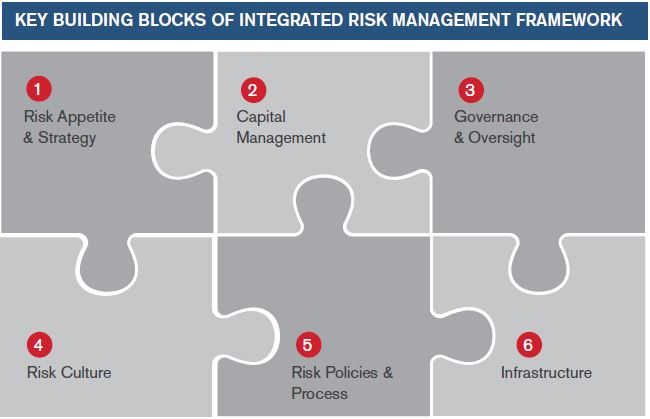

Risk Management at the Bank is underpinned by a set of key principles which serves as the foundation of the Bank’s risk management framework.

1

Establishment of a risk appetite and strategy which articulates the nature, type and level of risk, the Bank is willing to assume and is approved by the Board.

2

Capital management driven by the Bank’s strategic objectives and accounts for the relevant regulatory, economic and commercial environments in which the Bank operates.

3

Proper governance and oversight through a clear, effective and robust governance structure with well-defined, transparent and consistent lines of responsibility established.

4

Promotion of a strong risk culture that supports and provides appropriate standards and incentives for professional and responsible behavior.

5

Implementation of policies to ensure that risk management practices and processes are effective at all levels and execution of sound risk management processes to actively identify, measure, control, monitor and report risks inherent in all products, activities, processes, systems and exposures.

6

Ensure sufficient resources and systems infrastructure are in place to enable

effective

risk management.

Risk Appetite & Strategy

Risk Appetite is defined as the quantum of risk the Bank is willing to assume in different areas of business in achieving its strategic objectives and ensuring maintenance of desired risk profile. The Risk Appetite framework and Risk Tolerance limits have been defined by the Board in consultation with the Senior Management of the Bank in line with the Bank’s overall business strategy, providing clear direction to the business units for on-going operations and risk management. The Risk Appetite framework and Risk Tolerance limits are reviewed and adjusted by the Board when required based on developments in the operating environment.

In the event the risk appetite threshold has been breached, risk management and business controls are implemented to bring the exposure level back within the accepted range. Risk appetite, thus, translates into operational measures such as limits or qualitative checkpoints for the dimensions of capital, earnings volatility and concentration risk etc. In order to effectively implement risk appetite, the Bank has defined quantitative indicators (e.g., capital adequacy level and risk limits) or qualitatively embedded same in the policies and procedures (e.g., underwriting criteria).

Capital Management

Effective capital management is fundamental to the sustainability of the Bank. As such, the Bank pro-actively manages its capital position, capital mix and capital allocation to meet the expectations of key stakeholders such as regulators, shareholders, investors and rating agencies. Capital helps protect individual banks from insolvency, thereby promoting safety and soundness in the overall banking system. The Bank’s approach to capital management is driven by strategic objectives and guided by the Basel principles.

BASEL lll Framework

The Central Bank of Sri Lanka (CBSL) issued guidelines this year on Capital Requirements Basel III requiring banks to comply with same from 1 July 2017. Basel III capital standards endeavour to strengthen the quantity and quality of capital in banks. The Bank is fully compliant with these requirements. Details of compliance under each pillar are discussed below.

Pillar I – Minimum Capital Requirement

The objective of minimum capital requirements

under Pillar I of the Basel III framework is to

ensure that banks hold sufficient capital for

Credit, Market and Operational Risks. The

Bank is currently using the Standardized

Approach for minimum capital computation for

Credit Risk, the Standardized Measurement

Approach for minimum capital computation for

Market Risk and Basic Indicator Approach for

minimum capital computation for Operational

Risk. The Bank continues to maintain capital

well above the minimum requirement set by

the CBSL.

Credit Risk - With the intention of eventually moving to Internal Rating Based approaches the Bank rolled out rating models with the assistance of CRISIL Risk and Infrastructure Solutions Limited, India in 2014. CBSL is yet to issue guidelines for banks on Advanced Approaches of capital computation under Credit Risk.

Market Risk - The Bank has already rolled out its VaR models and will consider moving to advanced approach of capital computation for Market Risk on receipt of guidelines from the regulator.

Operational Risk - The Bank had been computing capital requirements in parallel as per The Standardized Approach (TSA) and Alternative Standardized Approach (ASA). The Bank forwarded a formal application to the CBSL requesting to grant approval to move to ASA after analyzing both advanced approaches (TSA & ASA) in considering the cost saving against the currently used Basic Indicator Approach (BIA).

Pillar ll – Supervisory Review Process

Minimum regulatory capital requirements

under Pillar l establishes regulatory capital

thresholds that banks should meet. The

Pillar II (Supervisory Review Process - SRP)

requires banks to implement an internal

process, called the Internal Capital Adequacy Assessment Process (ICAAP), for assessing

capital adequacy in relation to the risk

profiles as well as a strategy for maintaining

capital levels. The Pillar ll also requires

the supervisory authorities to subject all

banks to an evaluation process/Supervisory

Review Process (SRP), and to initiate such

supervisory measures, as might be considered

necessary. The Bank has in place an ICAAP

and has adhered to same from January 2013.

The ICAAP process has strengthened the risk

management practices and capital planning

process of the Bank.

The capital adequacy management framework serves to ensure that the Bank and its group entities are adequately capitalized in line with the risk profile, regulatory requirements and target ratios approved by the Board and to promote efficient use of capital to meet business requirements, strategic growth and shareholder return. The management framework further focuses on the financial ability of the Bank to absorb any potential losses that it might incur under varying market and economic conditions.

The Bank’s capital management objectives can be summarized as follows:

-

Maintain sufficient capital to meet minimum regulatory capital requirements

-

Hold sufficient capital to support the Banks’ risk appetite

-

Allocate capital to businesses to support the Bank and its group companies strategic objectives

-

Ensure that the Bank maintains capital in order to withstand the impact of potential stress events.

The Bank identified seventeen risks as material in line with the strategic plan. The choice is based on directions given by CBSL and self-assessment of most important risk categories which need a separate mention from an ICAAP perspective. The seventeen material risks identified are Credit Risk, Market Risk, Operational Risk, Concentration Risk, Interest Rate Risk in Banking Book, Liquidity Risk, Under-estimation of Credit Risk, Residual Risk, Strategic Risk, Reputational Risk, Legal Risk, Compliance Risk, Governance Risk, Model Risk, Settlement Risk, Group Risk and Cross-border Risk. These risk categories and their assessments are covered in detail in the ICAAP of the Bank.

The annual Capital Planning Process involves detailed planning of the strategic capital plan over at least a three-year horizon. The plan highlights the capital projections, capital requirements, levels of capital and capital mix to support the Bank’s business plan and strategic objectives. The Bank manages its capital structure and adjusts it accordingly in line with changes in local and global economic and market conditions and its overall risk appetite. Notwithstanding same, the projected capital plan is prepared considering mainly the organic growth, which assures adequate capital for the Bank for the next 3 years. The Bank and the Group would have the option to raise capital under normal and stressed scenarios by way of equity / capital infusion, issue of innovative perpetual debt instrument, issue of subordinated bonds or Hybrid capital instruments.

The Bank will continue to be proactive in its efficient utilization of capital and will constantly monitor ongoing developments affecting regulatory capital requirements as well as related capital market developments. The Bank is also committed to ensure continuous healthy capital levels with an optimal capital mix to support the Bank’s and the Group's strategic agenda and simultaneously maximizes value to shareholders.

The Bank has in place a comprehensive Stress Testing Policy and Framework in line with the regulatory guidelines as well as international best practices. The policy describes the purpose of stress testing and governance structure and the methodology for formulating stress tests whilst the framework specifies in detail the Stress Testing program including the stress tests, frequencies, assumptions, tolerance limits and remedial action.

Stress tests are conducted on standalone and consolidated basis at various frequencies in line with the Board approved framework and details of those are reported to Board IRMC. The outcome of the stress testing process is monitored carefully and remedial actions are taken in case of breaches. Further, stress testing is used by the Bank as a tool to supplement other risk management approaches.

The Stress Tests carried out as at 31.12.2017 are given below.

|

Credit Risk |

|

Impact of increase in the Non-Performing Assets on Capital Adequacy Ratio (CAR) |

|

Impact of change in Impairment on CAR |

|

Impact of default of Large Borrowers on CAR |

|

Credit Concentration Risk |

|

Impact of default by the Largest Group on CAR |

|

Impact of default in Specific Sector/Region on CAR |

|

Interest Rate Risk |

|

Impact of change in Interest Rates - Trading Book (Debt Securities) |

|

Impact of change in Interest Rates on CAR for Banking Book |

|

Exchange Rate Risk |

|

Impact of Exchange Rate movements of the Bank's (DBU and FCBU) Net Open position on CAR |

|

Impact of Exchange Rate movements of the Domestic Banking Unit (DBU) Net Open position on Profits |

|

Liquidity Risk |

|

Market Specific Stress Test - Adverse impact on Money Market & Institutional Borrowings/ Drop in Market Liquidity – DBU/FCBU on Liquid Asset Ratio (LAR) |

|

Bank Specific - Run down on CASA & Time Deposits –DBU/FCBU on LAR |

|

Market / Bank Specific - Adverse Impact on Total Liquid Liabilities – DBU/FCBU on LAR |

|

Impact of loss of large depositors on LAR |

|

Impact on CAR due to higher interest paid in a deposit run off scenario |

|

Combined Stress Test |

Pillar lll – Disclosures

The Bank provides enhanced quantitative and qualitative disclosures in line with the Basel III requirements in the Annual Report, website and press to provide a meaningful picture of the extent and nature of various risks that the Bank is exposed to and the Banks’ risk management practices.

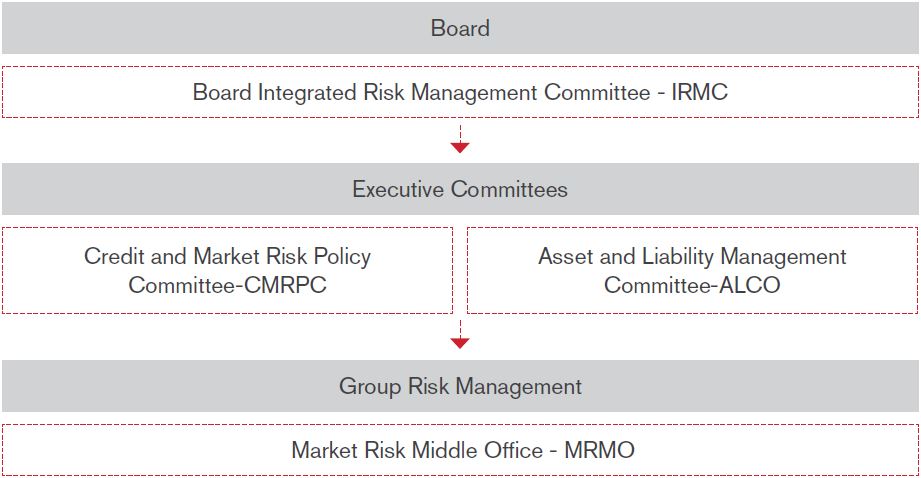

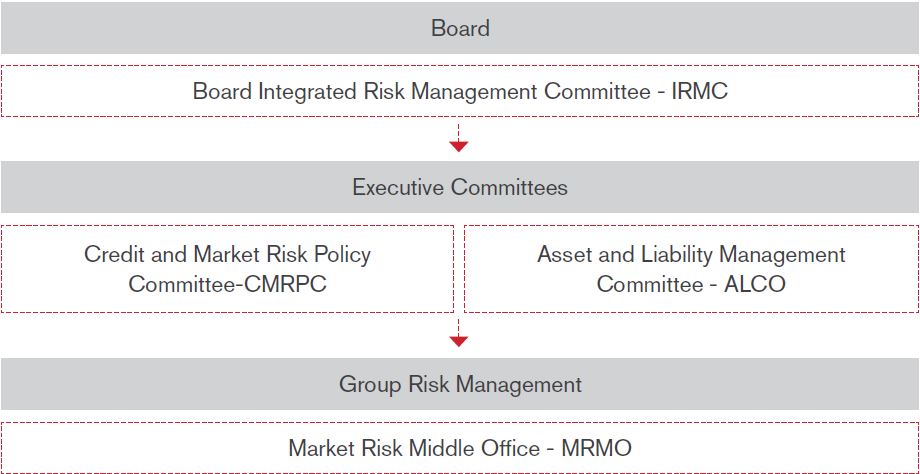

Governance and Oversight

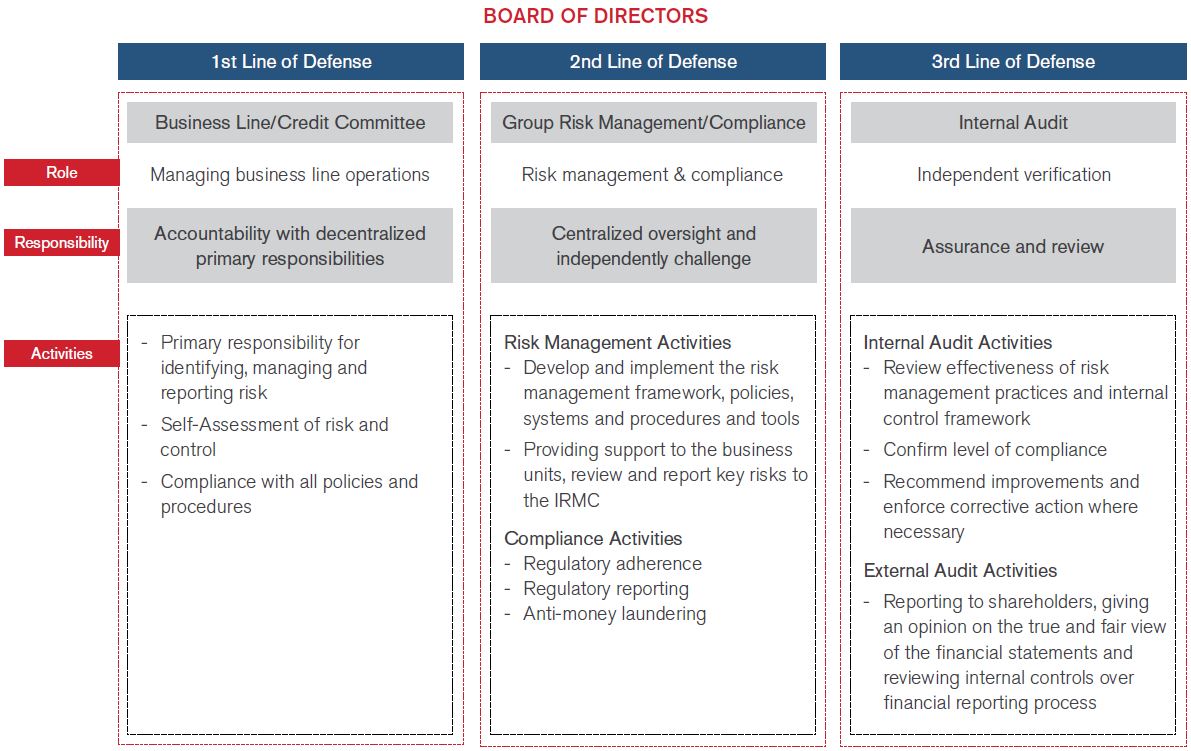

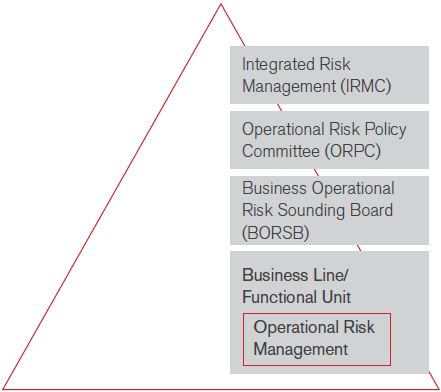

The Bank’s Board of Directors has the overall responsibility for risk management and sets the tone at the top for the effective management of risks through its risk appetite. In discharging its governance responsibility, it operates through two key committees, namely the Integrated Risk Management Committee (IRMC) and the Board Audit Committee (BAC) which have been formed in compliance with the CBSL Direction No. 11 of 2007 on Corporate Governance.

Governance Model

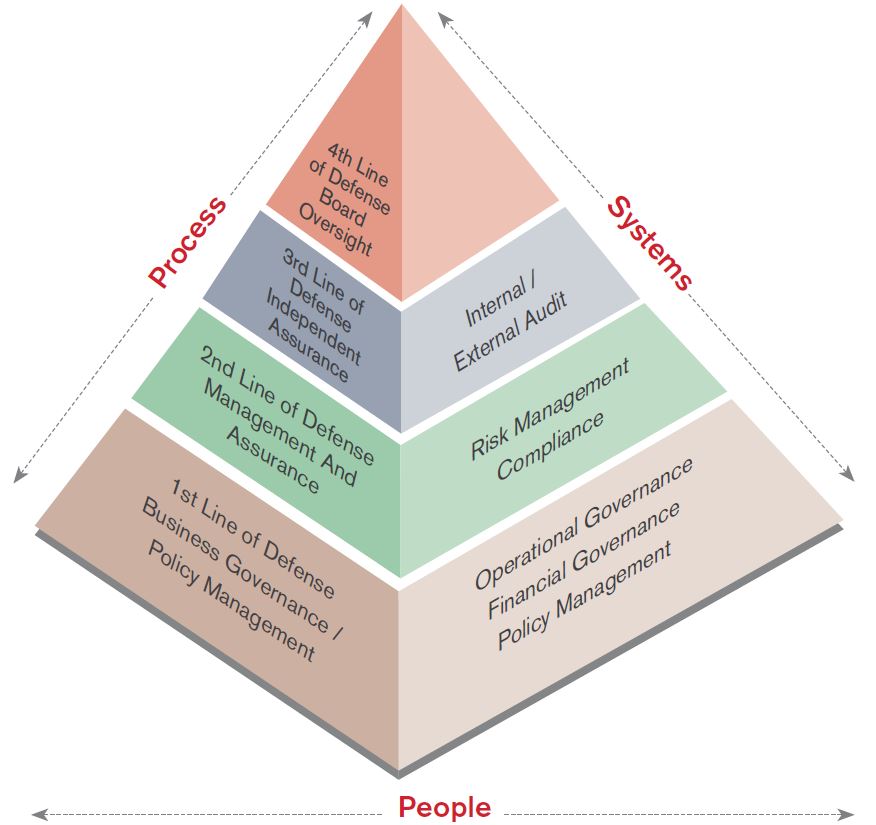

The governance model aims to place accountability and ownership, whilst facilitating an appropriate level of independence and segregation of duties. The structure is premised on the three lines of defense and defines the lines of authority, roles and responsibilities to efficiently manage risk across the Bank.

BOARD OF DIRECTORS

The ultimate governing body with overall risk oversight responsibility

BOARD SUB COMMITTEES

Integrated Risk Management Committee (IRMC)

Reviews the risk profile and policies of the Bank, its group companies and their application in the operations of the business in respect of the main risk categories viz. Credit Risk, Operational Risk, Liquidity Risk, Market Risk, Strategic Risk and Compliance, and ensures such risks are managed within the prudent levels decided by the Board of Directors.

Composition - Four Non-Executive Directors, CEO, CRO and Compliance Officer.

Board Audit Committee (BAC)

Assist the Board of Directors in its general oversight on financial reporting, internal controls and functions relating to internal and external audit.

Composition - Five members of the Board of Directors. The Vice President Group Audit functions as the Secretary to the Committee. The CEO, External Auditors and other members of the senior management attend meetings on invitation.

Board Credit Committee (BCC)

Reviews and approves Credit Proposals coming under the Committee’s delegated lending authority. Board of Directors.

Composition - Seven Non- Executive Directors and CEO.

BOARD SUB COMMITTEES

Credit and Market Risk Policy Committee (CMRPC)

Reviews the Bank’s risk policy framework, overall performance and the potential risks faced by specific lines of business and support functions.

Composition - CEO, CRO, Head of Credit Review, Heads of Business Units, Head of Treasury , Head of Credit Risk and Head of Market Risk.

Asset & Liability Management Committee (ALCO)

Reviews all Market and Liquidity related exposures on a monthly/more frequent basis and decisions are made to facilitate the business requirements and make pricing/ investment/policy decisions.

Composition - CEO, CRO, GCFO, Head of Treasury, Head of ALM and Heads of Business units.

Operational Risk Policy Committee (ORPC)

Monitors and ensures that an appropriate Operational Risk management framework is in place. Management of all aspects of operational risks and control lapses identified through the incident management process, internal audits and regulatory reviews whilst ensuring all significant issues raised are resolved within agreed timescales. Ensure full compliance of the local regulations. Raise awareness of new trends and developments in operational risk management techniques and migration to best practices. Assist the Bank in the management of Corporate Governance related to Operational Risk on an ongoing basis.

Composition - CEO, CRO, GCFO, Compliance Officer, Heads of Business Units, Heads of Support functions and Head of Operational Risk.

Group Risk Management

The Group Risk Management Division is independent of the business units and reports directly to the Integrated Risk Management Committee. Each unit within the Risk Management Division contributes to the management of risk and co-ordinates across the business functions to guarantee that risk management is impeccably integrated into the Bank’s corporate culture.

Further a Loan Review unit was formed within the Group Risk Management Division to carry out Loan Review Mechanism (LRM) activities as prescribed by the regulator. Its responsibilities extend to identifying potential problematic loans/facilities (post approval/granting) and providing rational, objective and professional recommendations for remedial action for implementation by line management.

In order to make the pre-approval process independent and with a view to further strengthen same the Credit Review Division which handles the pre credit review/approvals beyond specific thresholds also came under the purview of the Group Risk Management Division.

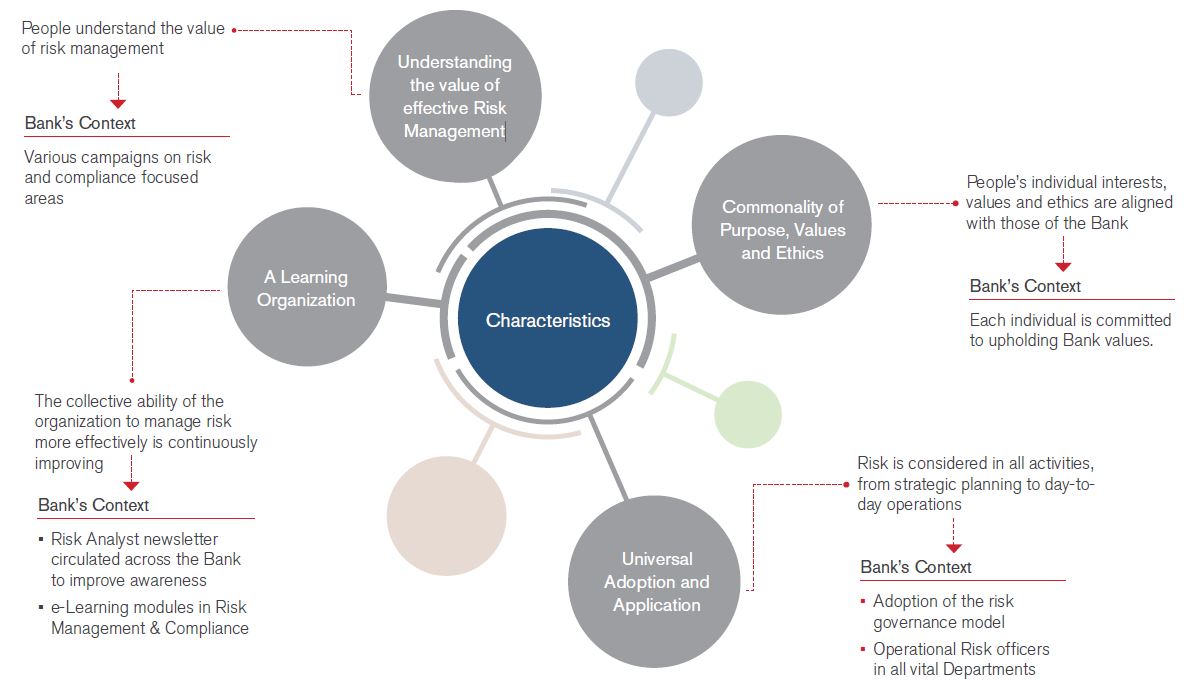

RISK CULTURE

A strong risk culture is the fundamental tenet of Bank’s risk management and serves as the foundation upon which a strong risk management structure is built. Within the Bank, the key characteristics of a strong risk culture are identified as follows:

In the Bank a compliance culture is instilled where the Board, Senior Management and every employee is committed to adhere to the requirement of relevant laws, rules and regulatory guidelines. The Bank's commitment is clearly demonstrated through the establishment of strong policies and guidelines and ensuring that non-compliance risks are effectively managed. Such measures not only ensure adherence to regulations, but also protect the Bank’s integrity and reputation.

Risk Policies & Processes

CREDIT RISK

Credit risk is the risk of financial loss if a customer or counterparty fails to meet a payment obligation under a contract. It arises principally from direct lending, trade finance and leasing business, and also from offbalance sheet products such as letters of credit and guarantees. Credit Risk generates the largest regulatory capital requirement of the risks we incur. The Bank manages the Credit Risk in the entire portfolio as well as individual credits or transactions.

Objectives Of Credit Risk Management

The objectives of Credit Risk Management are:

-

Ensure optimal risk-reward pay-off for the Bank and to maximize returns

-

Maintain the quality of the portfolio by minimizing the non-performing loans and probable losses

-

Maintain a well-diversified portfolio by prudently managing the risk in the asset portfolio to ensure that the risk of excessive concentration to any industry, sector or individual customer is minimized

-

Ensure that exposures to any industry or customer are determined by the regulatory guidelines, clearly defined internal policies, debt service capability and balance sheet management guidelines

-

Avoid all situations of conflict of interest and report all insider-related credits to appropriate bodies

1

A Well-Defined Credit Policy approved by the Board of Directors

-

Set the Credit culture of the Bank

-

Specify target markets for lending

-

Specify prohibited lending

-

Set acceptable risk parameters

-

Set remedial and recovery actions

2

Structured and Standardized Credit Approval

-

Credit is extended only to suitable and well-identified customers

-

Never to take a credit risk where ability of the customer to meet obligations is based on the most optimistic forecast of events

-

Risk considerations shall have priority over business and profit considerations

-

The primary source of repayment for each credit is from an identifiable cash flow from the counterparty’s normal business operations or other financial arrangements

-

Adopt a pricing mechanism that reflects variation in the risk profile of various exposures to ensure that higher risks are compensated by higher returns

-

The financial performance of borrowers is to be continuously monitored and frequently reviewed

3

Delegation of Authority

-

Two Credit Committees representing the Business Lines

-

The delegated authority limits are reviewed periodically and the Bank follows the four-eyes principle

-

Lending decisions are based on detailed credit evaluation

4

Delegation of Authority

-

System driven obligor risk rating, facility risk rating and retail score cards to suit the diverse client portfolios of the Bank

-

Incorporating both quantitative and qualitative parameters

5

Risk Pricing

-

Pricing of credit risk using scientific methods

6

Post Sanction Review and Monitoring

-

Warning signals are identified

-

Watch listing process in place

-

Non-performing assets are identified at an early stage

7

Prudential Limits

Maximum exposure limits on;

-

Single Borrower/Group Exposure limits

-

Prudential Group Exposure limits

-

Substantial Exposure limits

-

Industry/Economic Sector limits

8

Portfolio Management

-

Evaluates exposures on the basis of industry concentration, rating quality, internally established pre specified early warning indicators

-

Regular portfolio reviews, stress tests and scenario analysis

-

The exposures in off balance sheet products are treated with utmost care

9

Portfolio Management

-

Ways out analysis

-

Comprehensive and legally enforceable documentation

-

Obtaining of collateral in line with the Bank's policy and ensuring enforceability

10

Impairment

-

Board approved policy

-

Clearly defined process

Credit Policies

The Bank has a well-defined credit policy approved by the Board of Directors. It defines the

-

Credit culture of the Bank

-

Specify target markets for lending

-

Specify prohibited lending which the Bank under no circumstances will entertain due to either the very high risks involved in such proposals and / or its negative social / ethical consideration

-

Set acceptable risk parameters

-

Set remedial and recovery actions

Structured and Standardized Credit Approval Process

Depending on the nature of the project / product standardized formats have been designed and evaluations are carried out by competent staff. There are clear guidelines set to ensure that;

-

Credit is extended only to suitable and well-identified customers and never where there is any doubt as to their ethical standards and record, where the source of repayment is unknown or speculative nor where the purpose/destination of funds is undisclosed;

-

Never to take a credit risk where ability of the customer to meet obligations is based on the most optimistic forecast of events;

-

Risk considerations shall have priority over business and profit considerations;

-

Ensure that the primary source of repayment for each credit is from an identifiable cash flow from the counterparty’s normal business operations or other financial arrangements; the realization of security remains a fallback option;

-

Adopt a pricing mechanism that reflects variation in the risk profile of various exposures to ensure that higher risks are compensated by higher returns;

-

The financial performance of borrowers is to be continuously monitored and frequently reviewed, as is the manner in which the borrower operates his accounts.

Delegation of Authorit

Final authority and responsibility for all activities that expose the Bank to credit risk rests with the Board of Directors and the Board of Directors has delegated approval authority to the CEO to re-delegate limits to the Credit Committees and the Business Lines. All approval limits are name specific and are based on the individual experience, facility type and collateral in order to ensure accountability and mitigate any judgmental errors.

-

There are two Credit Committees representing the Business Lines and these Committees comprise senior officers of Business Lines and the Credit Review Division.

-

The delegated authority limits are reviewed periodically and the Bank follows the ‘foureyes principle’ (i.e. minimum of two officers signing a credit proposal).

-

Lending decisions are based on detailed credit evaluation carried out by Relationship Managers/ Credit Officers and reviewed/ approved by designated approving authority.

Internal Risk Ratings of Obligors

The Bank has an Internal Risk Rating system which runs on sophisticated work flow based software and hosts obligor risk rating, facility risk rating and retail score cards to suit the diverse client portfolios of the Bank. This move facilitates accurate quantification of credit risk, and also complies with Central Bank Direction No. 07 of 2011 on Integrated Risk Management.

The Bank has deployed varying models to gauge the default risk associated with Large Corporate, Mid Corporate, SME and Non-Banking Financial Institutes. All of these models are structured in a manner incorporating both quantitative and qualitative parameters to reflect the underlying probabilities of default.

The risk rating model implemented facilitates both obligor and facility rating. Whilst obligor rating will indicate the expected probability of default (PD), the facility rating indicates the expected loss given default (LGD). Expected probability of default takes into account the characteristics of the obligor assessed via industry, business, management and financial risk silos, whilst facility rating takes into account the type of the facility, nature of the collateral and realizability. Using the expected probability of default and the loss given default calculated via obligor rating and facility rating models the system facilitates arriving at an expected loss for a specific credit.

Risk Scoring

The Bank deploys custom made scorecards to underwrite consumer assets. The scorecards take into account the customer demographics together with creditworthiness of individuals and disposable income in deciding the level of accommodation of credit. In addition to above, the Bank also carries out a prescreening of employers of salaried employees who seek consumer credit from the Bank in order to ensure that their level of income generation will not get interrupted in the foreseeable future. In this way the Bank acts more responsibly as such an approach would negate possibility of overspending by consumers based on uncertain future income.

Risk Pricing

The Bank also views pricing for risk as fundamental to Credit Risk Management. Thus steps have been taken to price the credit risk using more scientific methods. A risk based pricing model has been rolled out across the Bank .

Post Sanction Review and Monitoring Mechanism

Post sanction review and monitoring is carried out to ensure quality of credit is not compromised. Any deteriorating credits with emphasis on internal and external early warning signals are identified and such accounts are “Watch Listed”. The Watch Listed clients are monitored closely with quarterly reports submitted to the Credit Committees. Further, based on the Watch Lists the Bank assesses the Portfolio at Risk in the event, such accounts deteriorate further. Non-performing assets are identified at an early stage, enabling management to take action as appropriate.

Prudential Limits

The industry and portfolio limits are set by the Board of Directors on the recommendation of the Group Risk Management Department. Credit Risk Management monitors compliance with approved limits. Desired diversification is achieved by setting maximum exposure limits on

-

Single / group obligor exposures - limits are more stringent than the limits set by the regulator and on a prudential basis, the off- balance sheet items are considered at face value instead of credit equivalent of such exposures

-

Prudential Group exposures - considered based on the Bank’s exposure to a ‘Group of Related Parties' and is capped at 60% of the Bank’s Capital Base

-

Substantial exposures – this is in compliance with the Banking Act Direction No 07 of 2011 on Integrated Risk Management Framework for Licensed Banks and the Bank has introduced a substantial exposure limit of 500% of the capital base of the Bank

-

Industry/economic sector exposures - limits are imposed for lending to different sub- sectors in the economy. This is a control mechanism introduced recognizing that during various economic cycles, different sectors of the economy could face difficulties. At present the limit for a sub sector is set at 15%.

Portfolio Management

Credit portfolio management is an important function within the overall credit risk management function. Need for such critical and objective portfolio management emanates from the need to optimize the benefits associated with diversification. It also helps the Bank to identify and address potential adverse impact of concentration of exposures. The Bank has a well-structured portfolio management mechanism which evaluates exposures on the basis of industry concentration, rating quality, internally established pre specified early warning indicators apart from regulator imposed quantitative ceiling on the single borrower and aggregate exposure. The Bank’s internal single borrower and Group exposure limits are much stringent than those imposed by the regulator. Based on the feedback from the credit portfolio management, the credit origination criterion is amended prudently to insulate portfolios from further deterioration.

The portfolio management team also undertakes, apart from regular portfolio reviews, stress tests and scenario analysis when the external environment, both local and global, undergoes significant changes. Credit portfolio management envisages mitigating credit risks to a great extent by stipulating prudential risk limits on various risk parameters. As such, the Bank has established single borrower limit, limits for related party borrowings and aggregate limit for large exposures as prescribed by the regulators. Moreover the Bank has also established maximum limits to different industry segments. Such limits are clearly spelt out in the credit policy and the authority for permitting any deviations on an exceptional basis is also clearly documented. The Bank adopts a similar mechanism to assess the risks associated with off balance sheet exposures. As part of the credit portfolio management and monitoring procedures, the exposures in off balance sheet products such as FX Forwards, Guarantees and Letters of Credit are treated with utmost care.

KRIs supplement the overall portfolio management system, by providing a view of the credit risk of the portfolio as well as acting as an early warning system. Some of the KRIs monitored and reported to Board Integrated Risk Management Committee are given below;

|

Portfolio of the Bank Industry portfolio |

To assess the trends in comparison with industry and measure performance against budgets/Risk Appetite |

|

Market Share |

|

|

NPLs of the Bank Industry NPLs |

|

|

NPL Ratio of the Bank Industry Average NPL Ratio |

|

|

Impairment - Cumulative Charge - Individual Impairment % - Total Impairment against portfolio |

|

|

Provision Cover - % of the Bank Industry % |

|

|

Open Loan Position |

|

|

ROE % |

|

|

Tier I Capital Adequacy Ratio % |

To assess compliance with Regulatory limits and the Bank’s Risk Appetite |

|

Tier I + Tier II Capital Adequacy Ratio % |

Credit Risk Mitigation

The Bank adopts various mechanisms to mitigate the credit risk of the loan book.

-

Ways out analysis - the primary source is established through a conservative evaluation of whether the borrower's realistic projected cash flows will be sufficient to repay their debts. This is further mitigated by a second way out in the event of unforeseen adverse circumstances and availability of collateral alone does not make an unacceptable proposal viable. Exemptions on collateral are allowed in the event the borrower demonstrates strong and reliable financial performance.

-

Documentation of credit transactions with adequate terms, conditions and covenants in a comprehensive and legally enforceable basis.

-

Obtaining of collateral in line with the Bank's policy and ensuring it is supported by enforceable documentation. Collateral policy differs from business line to business line according to the products offered.

The main types of collateral taken by the Bank are

-

immovable property mortgages,

-

plant, machinery and equipment,

-

cash deposits,

-

mortgages on stocks and book debts and

-

corporate and personal guarantees.

-

It is the Bank's policy to be on a pari passu status with other lenders in terms of collateral cover. A decision to the contrary may be acceptable only where a non pari passu position is accepted due to unavailability of security as a result of the Bank being a late entrant to the relationship and is supported by strong financial position of the entity financed. Facilities under Product Programmes are governed by guidelines given in such individual programmes.

In instances where facilities are granted without collateral, the Bank ensures that its position will not be subordinated to other creditors’ interests. In such instances, the Bank generally requires either a negative pledge agreement not to encumber any assets without permission of the Bank or a pari passu clause, whereby the debtor will treat the Bank equally with respect to collateral with all current and future lenders.

The Bank has a panel of valuers who have been selected based on the criteria set out by the Central Bank of Sri Lanka. The Bank ensures that the valuations are carried out and reviewed as following.

-

Facilities in NPL:

-

In respect of credit facilities granted against residential property which is occupied by the borrower for residential purposes – every 4 years

-

In respect of credit facilities granted for all other purposes – every 3 years

-

-

Performing facilities:

-

Watch listed clients with working capital facilities - every 3 years

-

Other Clients with working capital facilities - every 5 years

-

No value is considered if valuations are not in line with the time frames set out as per the CBSL guidelines.

Impairment

The Bank has in place a detailed impairment policy which was approved by the Board of Directors. A credit risk provision for loan impairment is established if there is objective evidence that the Bank will be unable to collect all amounts due on loans and advances according to the original contractual terms.

Objective evidence that a loan is impaired includes observable data that comes to the attention of the Bank about the following loss events:

-

Significant financial difficulty of the customer

-

A breach of contract such as default of payment

-

A breach of contract such as default of payment

-

Where the Bank grants the customer a concession due to the customer experiencing financial difficulty

-

It becomes probable that the customer will enter bankruptcy or other financial reorganization

-

Observable data that suggests that there is a decrease in the estimated future cash flows from the loans, to name a few.

The Bank determines the allowances appropriate for each individually significant loan or advance on an individual basis if there is any objective evidence of a loss based on the above. Items considered when determining allowance amounts include

-

The sustainability of the counterparty’s business plan/cash flows,

-

Projected receipts and the expected payout should bankruptcy ensue,

-

The realizable value of collateral and the timing of the expected cash flows.

A provision for impairment of loans is reported as a reduction of the carrying amount of loans on the balance sheet. Additions to provisions for loan impairment are made through impairment losses on loans and receivables in the income statement.

All exposures are assessed for impairment either individually or collectively. If there is objective evidence of incurred loss individually i.e. for exposures which are considered to be individually significant (exposures above LKR 50 million), the exposure should be measured for an impairment provision. If it is determined that no objective evidence of incurred loss exists for an individually assessed exposure, that exposure should be included in a group of exposures with similar credit risk characteristics that are collectively assessed for impairment.

If there is objective evidence that an impairment loss on loans and receivables carried at amortized cost has been incurred, the amount of the loss is measured as the difference between the loans’ carrying amount and the present value of estimated future cash flows discounted at

-

the loan’s original effective interest rate, if the loan bears a fixed interest rate, or

-

current effective interest rate, if the loan bears a variable interest rate.

The estimation of the recoverable amount of a collateralized exposure reflects the cash flows that may result from Liquidation of Collateral where foreclosure is considered the likely course of action. The time, costs and difficulties involved in obtaining repayment through collateral should be taken into account when determining the recoverable amount.

For the purposes of a collective evaluation of impairment, loans are grouped on the basis of similar credit risk characteristics. Corporate and SME loans are grouped based on product type, economic sector and on days in arrears. Retail Banking loans are grouped based on product type and number of days in arrears. Those characteristics are relevant to the estimation of historical loss experience for loans. Historical loss experience is adjusted on the basis of Probability of Default and Loss Given Default. The Bank also bases its analyses on economic factors and portfolio factors such as :-

-

Macro Economic Factors such as

-

Interest rate stability

-

Unemployment rate

-

Inflation

-

GDP growth rate

-

Exchange Rate fluctuation

-

-

Portfolio Factors such as

-

Rescheduled Loans as a % of total Loans

-

Average Age of the portfolio

-

Management's judgment on delinquencies of the borrowers

-

-

Other Factors such as

-

Sovereign ratings assigned to Sri Lanka by local and international rating agencies

-

Global Economic Environment which has direct impact to the Sri Lankan economy

-

Borrower's ratings assigned by local and international rating agencies

-

The Bank may use the aforementioned factors as appropriate to adjust the impairment allowances. Allowances are evaluated separately at each reporting date with each portfolio.

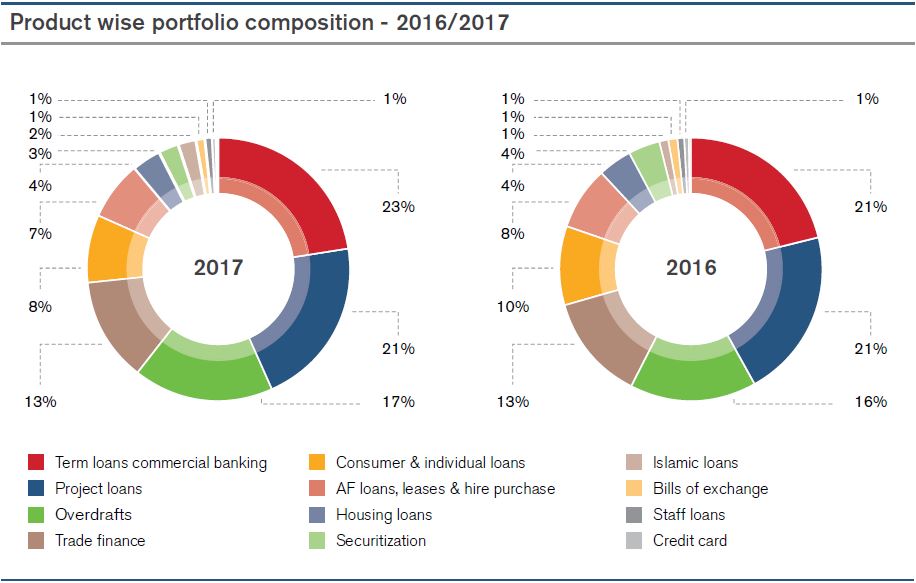

Credit Risk Analytics

Portfolio MixProduct Concentration

The Bank’s portfolio continues to be concentrated in working capital financing facilities and Project Loans.

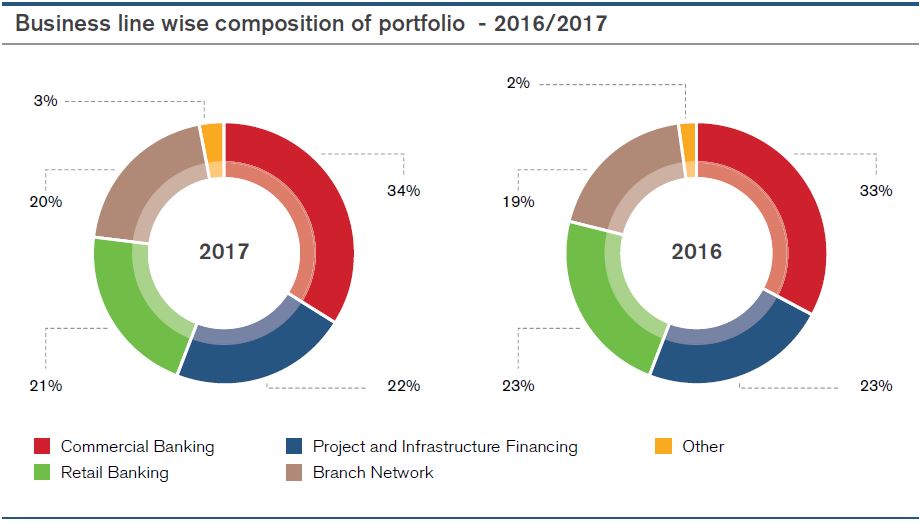

Business Line wise Composition

Business line wise composition of portfolio changed during the year in line with the long term strategy of the Bank.

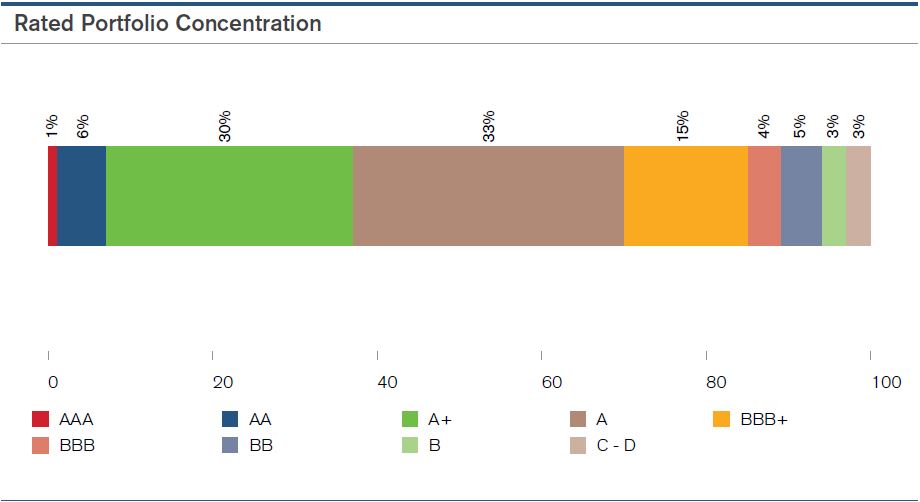

Rated Portfolio Concentration

The Bank’s rated portfolio continues to be concentrated on “A” rated clients based on the internal rating models used by the Bank to rate Corporate and SME clients and the composition was within the risk appetite of the Bank set by the Board.

Credit Risk Concentrations

Single Name Concentration

-

The Bank was in compliance with regulatory limits on Group and Single Borrower concentrations. The Bank was also in compliance with the internal limits set by the Board on Group and Single Borrower concentrations which are more stringent than those prescribed by the regulator.

-

The substantial exposures of the Bank accounted for only 132% of the capital base and was well within the internal limit.

-

The Bank’s portfolio concentrations were well within the risk appetite of the Bank set by the Board.

Sector Concentration

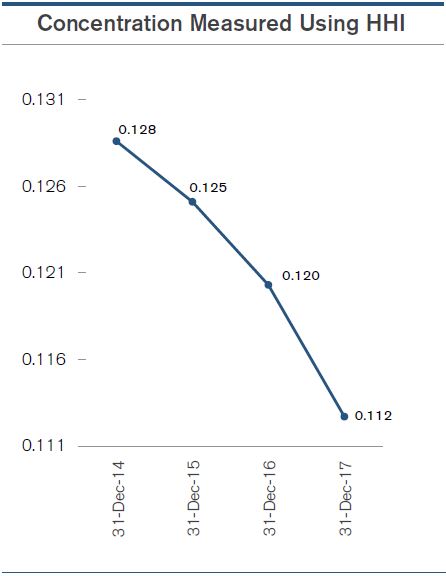

The Bank maintained a well-diversified portfolio and the portfolio was not over concentrated on a particular sector. The Bank was also in compliance with the minimum lending requirement of 10% to Agricultural sector. Bank measures the sector wise concentration risk using the Herfindhal-Hirschman Index and the trend indicated a reduction in concentration risk.

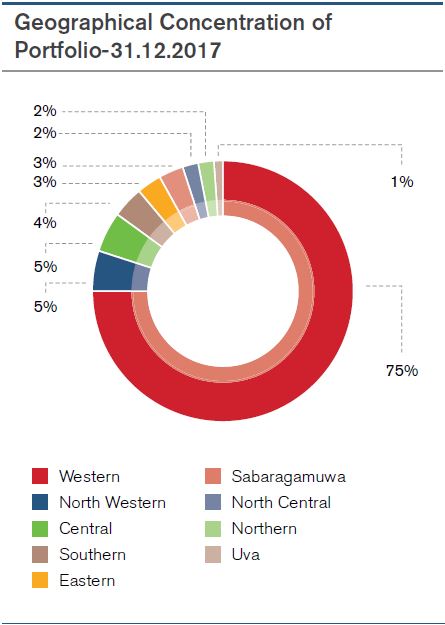

Geographical Concentration

Based on the economic activity highest concentration of domestic portfolio was in Western Province though the branch network is spread throughout the country. In line with Bank's strategy 96% of portfolio was concentrated locally.

NPL Analysis

Non-Performing Loans

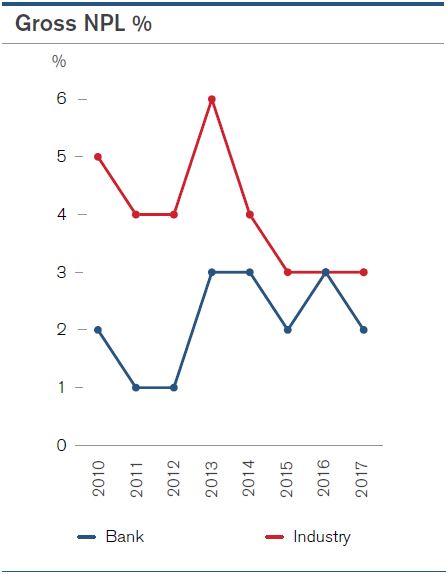

The Bank’s NPL ratio was well below the industry ratio reflecting a better quality portfolio than most players in industry.

NPL and Regulatory (CBSL) Provisioning on Balance Sheet Exposures as at 31 December 2017

|

(LKR '000) |

|

|

General Provision |

1,125,563.96 |

|

Non Performing - Specific Provisions |

2,470,896.62 |

|

Charges |

17,720.91 |

|

Total Specific Provision on NPLs |

2,488,617.53 |

|

Performing - Judgmental-Specific Provisions |

93,127.77 |

|

Total Loan Loss Provision |

3,707,309.26 |

|

|

NPL Amount LKR ‘000 |

Provisions as at 31 December 2017 |

Collateral Value considered for Provisioning purposes |

Net Exposure |

|

Pawning |

|

|

|

|

|

Special Mention |

602.70 |

- |

- |

602.70 |

|

Substandard |

131.60 |

26.32 |

- |

105.28 |

|

Doubtful |

17.00 |

8.50 |

- |

8.50 |

|

Loss |

989.96 |

989.96 |

- |

- |

|

Housing |

|

|

||

|

Special Mention |

69,597.93 |

- |

- |

69,597.93 |

|

Substandard |

24,733.60 |

4,946.72 |

- |

19,786.88 |

|

Doubtful |

3,645.01 |

1,822.50 |

- |

1,822.50 |

|

Loss |

73,985.90 |

43,188.64 |

30,797.26 |

30,797.26 |

|

Consumer Loans |

|

|

|

|

|

Special Mention |

77,073.23 |

- |

- |

77,073.23 |

|

Substandard |

24,157.88 |

4,831.58 |

- |

19,326.31 |

|

Doubtful |

35,040.61 |

17,520.31 |

- |

17,520.31 |

|

Loss |

203,355.81 |

203,355.81 |

- |

- |

|

Leases and Hire Purchase |

|

|

|

|

|

Special Mention |

368,048.67 |

- |

- |

368,048.67 |

|

Substandard |

82,964.49 |

16,592.90 |

- |

66,371.59 |

|

Doubtful |

16,197.76 |

8,098.88 |

- |

8,098.88 |

|

Loss |

96,224.43 |

96,224.43 |

- |

- |

|

Credit Card |

|

|

|

|

|

Special Mention |

5,970.36 |

- |

- |

5,970.36 |

|

Substandard |

33,261.71 |

8,315.43 |

- |

24,946.29 |

|

Doubtful |

25,816.66 |

12,908.33 |

- |

12,908.33 |

|

Loss |

97,860.18 |

97,860.18 |

- |

- |

|

Working Capital Facilities |

||||

|

Special Mention |

282,125.16 |

- |

- |

282,125.16 |

|

Substandard |

26,241.57 |

5,248.31 |

- |

20,993.25 |

|

Doubtful |

34,166.01 |

17,083.00 |

- |

17,083.00 |

|

Loss |

501,143.42 |

501,143.42 |

- |

- |

|

Term Loans |

|

|

|

|

|

Special Mention |

345,157.43 |

- |

148,156.22 |

345,157.43 |

|

Substandard |

262,946.48 |

16,195.52 |

54,459.67 |

246,750.95 |

|

Doubtful |

373,897.11 |

48,904.39 |

276,022.70 |

324,992.72 |

|

Loss |

880,931.33 |

799,754.97 |

57,539.22 |

81,176.37 |

|

Overdraft Facilities |

|

|

|

|

|

Special Mention |

241,360.13 |

- |

1,014.50 |

241,360.13 |

|

Substandard |

287,377.46 |

43,870.58 |

56,272.56 |

243,506.87 |

|

Doubtful |

144,060.49 |

62,827.70 |

18,940.65 |

81,232.79 |

|

Loss |

357,921.82 |

349,636.57 |

53,167.73 |

8,285.25 |

|

Other |

|

|

|

|

|

Special Mention |

1,097.23 |

- |

- |

1,097.23 |

|

Substandard |

- |

- |

- |

- |

|

Loss |

109,541.65 |

109,541.65 |

- |

- |

|

|

5,087,642.81 |

2,470,896.62 |

696,370.51 |

2,616,746.19 |

MARKET RISK

Market risk is the potential loss in both ‘On’ and ‘Off’-balance sheet positions arising from the movements in foreign exchange rates, interest rates, equity and commodity prices.

Objectives of Market Risk Management

The primary objective of Market Risk Management (MRM) is to ensure that Business units of the Bank optimize the risk-reward relationship within the Bank’s pre-defined risk appetite and avoid exposing the Bank to unacceptable losses.

Under a well-defined risk governance structure, the risks are identified, assessed, controlled and reported to ensure that the Bank operates within the allocated risk appetite levels. The Treasury activities are the key elements of Market Risk in the Bank, whilst other banking activities like deposit taking and lending activities forms a significant contribution over the same. The Treasury functions are segregated into three areas namely; Treasury Front Office, Market Risk Middle Office (MRMO) and Treasury Back Office where each unit has separate reporting lines to maintain independency. Treasury front office staff is guided by the Board approved Market and liquidity risk policies / limit framework and the Treasury Front Office Procedure guidelines. The procedure guideline provides the code of conduct for dealing room staff including the course of action to be taken in case of a violation of the rules and regulations stipulated therein.

Market Risk Governance Structure

Policies

Risk monitoring is guided by a well-defined policy framework and limit structure designed to suit the business model and the balance sheet structure reflecting the risk appetite of the Bank. The Board supported by Integrated Risk Management Committee (IRMC) approves the risk parameters as recommended by the Asset and Liability Committee (ALCO) and Market Risk Middle Office (MRMO)to facilitate the business needs.

The risk management policy framework covers the Market, Liquidity, Asset and Liability risk management guidelines on the procedure and techniques for assessing, managing, monitoring and reporting of risks related therein. The policy framework consists of the roles and responsibilities, procedures, risk measurement framework, risk monitoring, reporting and controls taking into account the rules and regulations and the best industry practice.

Processes

The key functions of Market Risk Management include Policy formulation, Risk Measurement methodologies, systems, control, reporting and communication. This will provide guidance on procedure for Market risk Management within the overall risk appetite of the Bank.

Policy Formulation |

|

Policy formulation/ renewal are carried out considering the regulatory guidelines, best practice in the market and material changes in Market Risk Management/ Limit monitoring process |

Risk Measurement Methodologies |

|

Limits are assessed and recommended to ALCO / Board approval. All limits in force will be independently monitored by MRMO on pre-defined time bands |

Systems and Controls |

|

Support in implementation of management reporting systems to accurately reflect the risks taken by the Bank. Develop, implement, and review the controls that enforce the adherence to established risk limits. |

Risk Reporting and Communication |

|

MRMO risk activities are identified and monitored on a timely manner against the risk parameters and where necessary the exposures are reported for senior management/ Board for necessary action. |

The Market Risk reports are circulated at a number of frequencies - daily, weekly, monthly and quarterly basis to Treasury, Senior Management, ALCO, IRMC and Board for decision making.

ALCO as the key Management Committee that regularly monitors the Market Risk exposures initiates appropriate actions to optimize the Risk exposures within the Risk appetite of the Bank.

The implementation of the Bank’s Market Risk Management policies, procedures and systems are delegated to the Head of Market Risk Management/Middle Office who reports to the Chief Risk Officer. Market and liquidity risks are addressed at ALCO on a monthly basis and at the IRMC level on a monthly/ quarterly basis.

Analytics

MRMO uses a range of techniques to measure the risk exposures arising from Treasury/general banking activities. In accordance with the economic and regulatory requirements, we measure, monitor and control the Bank’s exposures to market risk, given the size, complexity and risk profile of the Bank.

Prudential internal limits have been defined for exchange rate risks, interest rate risk and Price risks for close monitoring of exposures including various techniques such as Mark to Market, sensitivity analysis, Value at Risk (VaR) calculations and Stress testing. The exposure limits are linked to the Bank’s capital base/ balance sheet size/profitability as appropriate to ensure adequate and efficient capital allocation and planning.

Foreign Exchange Risk

Foreign exchange risk is the risk of losses arising through holding of assets and liabilities in foreign currency and due to the movements in foreign exchange rates against the base currency. The Bank is exposed to foreign exchange risk when it's on and off balance sheet assets and liabilities are not equal in a given currency or when the timing and certainty of the inflows and outflows differ.

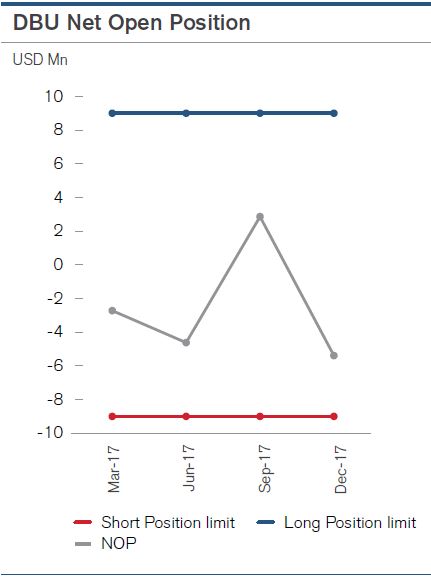

The Bank monitors the daily foreign exchange (FX) open positions to ensure that the Bank is operating within the regulatory limit on Net Open Position as depicted in the graph. Apart from the regulatory limit, the Bank has set internal prudential forex limits consisting of daily forex turnover limit, daylight position limit, forex gap limits, stress testing limits, sensitivity analysis, Swap funding limit and stop loss limits to closely monitor and mitigate foreign exchange risk.

The below table shows the Bank’s consolidated Foreign Exchange position and the exposure held against the Bank’s capital base which is managed well within the regulatory limit of 30%.

|

Foreign Exchange Position |

(DBU & FCBU) |

as at 31.12.2017 |

‘000 |

|||||

|

Currency |

Net AL Position |

Net Spot Position |

Net Forward Position |

Net Open Position |

Net Position in other Exchange Contracts |

Overall Exposure in Respective Foreign Currency |

Absolute Positions in USD Equivalent |

Overall Exposure in LKR |

|

US Dollars |

94,522.15 |

(2,348.64) |

(97,658.92) |

(5,485.42) |

0.00 |

(5,485.42) |

5,485.42 |

839,817.13 |

|

Pound Sterling |

(16,299.60) |

0.00 |

16,303.66 |

4.06 |

0.00 |

4.06 |

5.46 |

835.84 |

|

Euro |

(18,134.79) |

(12.27) |

18,100.45 |

(46.61) |

0.00 |

(46.61) |

55.68 |

8,524.43 |

|

Japanese Yen |

(31,144.03) |

0.00 |

28,306.24 |

(2,837.79) |

0.00 |

(2,837.79) |

25.17 |

3,852.77 |

|

Australian Dollar |

(18,613.30) |

0.00 |

18,620.92 |

7.63 |

0.00 |

7.63 |

5.94 |

910.09 |

|

Canadian Dollar |

(13.23) |

0.06 |

0.00 |

(13.18) |

0.00 |

(13.18) |

10.49 |

1,605.57 |

|

Other currencies |

(3,533.53) |

(475.00) |

4,818.67 |

810.14 |

0.00 |

810.14 |

248.48 |

38,042.35 |

|

Total Exposure |

893,588.19 |

|||||||

|

Total capital funds as per the latest audited financial statements |

28,737,835 |

|||||||

|

Total exposure as a % of total capital funds (should not exceed 30%) |

3.11% |

|||||||

Value at Risk (VaR)

VaR is a quantitative measure of the potential loss in value due to market movements which is expected for a defined period of time and a confidence level. The Bank’s Foreign exchange trading portfolio is subject to VaR measurement under historical simulation method on a daily basis. As prescribed by the Basel guidelines we calculate the VaR, using 99% confidence level for a one day holding period.

Value at Risk (VaR) on Forex Trading Portfolio

|

VaR - (at 99%) |

as at 31.12.2017 LKR million |

as at 31.12.2016 LKR million |

|

Forex Trading |

2.24 |

4.37 |

Historical approach, 1 day holding period

Stress Testing on DBU Net Open Position

Stress testing on Forex NOP under different magnitudes of shocks are performed to assess the impact on profitability as given below.

The Bank's Foreign Currency DBU Net Open Position and Stress Test Results as at 31.12.2017.

|

|

Net Position |

Scenario 1 |

Scenario 2 |

Scenario 3 |

Scenario 4 |

|

Magnitude of Shock (adverse) |

|

5% |

10% |

15% |

25% |

|

Spot Rate movement |

153.40 |

145.73 |

138.06 |

130.39 |

115.05 |

|

Net Open Position -DBU, Profit/loss (LKR) |

(5,396,107) |

41,388,143 |

82,776,285 |

124,164,428 |

206,940,713 |

Sensitivity Analysis

Daily sensitivity analysis is carried out on major foreign currency Net Open Positions (NOP) giving positive and negative shocks to the spot rates to determine the impact of exchange rate movements by way of profit or loss to the Bank’s income statement.

Exchange Rate Sensitivity of Major Foreign Currency Net Open Positions as at 31 December 2017.

|

Spot Rate Shocks |

LKR depreciate |

LKR appreciate |

||||||

|

Currency |

Net Open Position |

-5% |

-2.5% |

-1% |

Spot rate |

1% |

2.50% |

5% |

|

USD |

(5,485,416) |

(42,073,138) |

(21,036,569) |

(8,414,628) |

153.40 |

8,414,628 |

21,036,569 |

42,073,138 |

|

GBP |

4,056 |

42,069 |

21,035 |

8,414 |

207.42 |

(8,414) |

(21,035) |

(42,069) |

|

EUR |

(46,614) |

(429,654) |

(214,827) |

(85,931) |

184.34 |

85,931 |

214,827 |

429,654 |

|

JPY |

(2,837,788) |

(193,153) |

(96,577) |

(38,631) |

1.36 |

38,631 |

96,577 |

193,153 |

|

AUD |

7,626 |

45,808 |

22,904 |

9,162 |

120.14 |

(9,162) |

(22,904) |

(45,808) |

|

Total (LKR) |

|

(42,608,068) |

(21,304,034) |

(8,521,614) |

|

8,521,614 |

21,304,034 |

42,608,068 |

Interest Rate Risk (IRR) is the exposure of an institution's financial condition to adverse movements in interest rates. Changes in interest rates also affect the underlying value of the banking institution's assets, liabilities and off-balance sheet instruments, as the present value of future cash flows (and in some cases the cash flows themselves) change when interest rates change. Interest rate risk inherits various components; Re-pricing risk, basis risk, yield curve risk, option risk and price risk.

In order to manage the IRR, Bank has separated the balance sheet into trading and banking books. While the assets in the trading book (held for trading) are held primarily for generating profit through short term differences in prices/yields, the banking book (available for sale: AFS, held to maturity and loans and receivables) comprises assets and liabilities, which are contracted basically for steady income generation and are generally held till maturity. Thus, while the price risk is the prime concern of banks in the trading book, earnings or economic value changes are the main focus of the banking book.

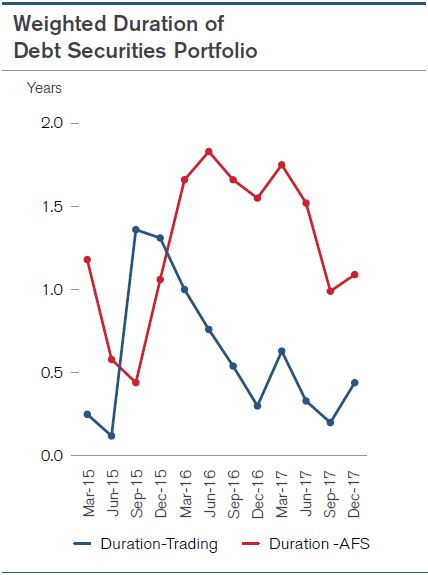

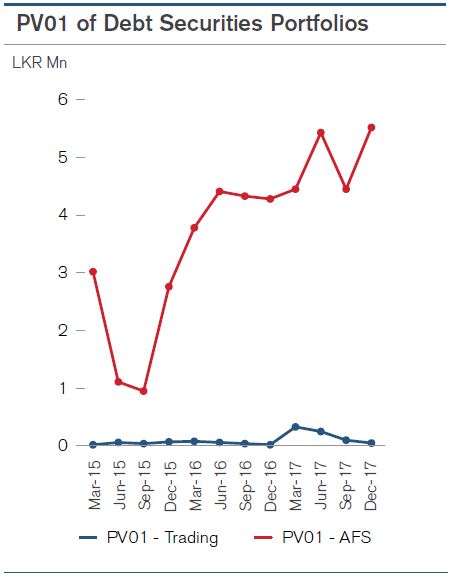

The Bank’s trading portfolio mainly comprises securities (Treasury Bills/Bonds), and is monitored daily against the portfolio size limit, duration limit, maturity mismatch limit and mark to market limits. Portfolios are subject to VaR (Value at Risk) and PVBP analysis to analyze the impact on fluctuations in interest rates which are being closely monitored to take advantage of the market movements.

|

Key Indicators |

Limit |

Position as at 31.12.2017 |

|

Mark to Market of Debt Trading Portfolio |

LKR (60) million |

LKR 4.57 million |

|

Duration of Debt securities - HFT |

2 Years |

0.44 |

|

Duration of Debt securities - AFS |

5 Years |

1.09 |

Value at Risk (VaR) on Treasury Bills/Bonds Trading and Available for Sale (AFS) Portfolio

|

VaR - (at 99%) |

as at 31.12.2017 |

as at 31.12.2016 |

|

Debt Securities - HFT |

0.36 |

0.28 |

|

Debt Securities - AFS |

29.79 |

25.33 |

Historical approach, 1 day holding period

Interest Rate Risk in the Banking Book (IRRBB)The IRRBB arises mainly through non-trading asset and liabilities such as loans and advances, which is measured and managed through price sensitivity /duration/ NII and variance analysis, and the interest rate sensitivity gap analysis.

Interest Rate Sensitivity Gap AnalysisThe Bank monitors the interest rate sensitivity of assets and liabilities using re-pricing gap report (Disclosure note No. 56.2 (C)).

The price sensitivity (Economic value perspective) of the Balance Sheet is managed within the risk parameters whilst maximizing the market potential on interest sensitive assets and liabilities.

Duration Analysis

PV01 Analysis

Modified Duration & Price Sensitivity of Local Currency Assets and Liabilities

As at 31 December 2017

|

|

Duration |

Total Balance |

Price Sensitivity |

|

LKR million |

|

||

|

Assets: |

|||

|

Overdrafts - LKR |

2.65 |

42,563.23 |

1,126.32 |

|

Credit Cards |

2.65 |

1,611.35 |

42.64 |

|

Margin Trading |

2.65 |

31.05 |

0.82 |

|

Term Loans - LKR |

0.31 |

23,245.09 |

72.13 |

|

Project Loans Fixed |

1.44 |

27,439.68 |

394.33 |

|

Project Loans Adjustable |

0.07 |

30,795.01 |

20.64 |

|

Refinance loans |

0.87 |

15.48 |

0.14 |

|

Securitization Loans |

0.73 |

8,267.57 |

60.55 |

|

Post Import Finance - LKR |

0.12 |

13,536.81 |

16.65 |

|

Packing Credit - LKR |

0.10 |

35.10 |

0.04 |

|

Trade Bills - LKR |

0.13 |

55.79 |

0.07 |

|

DM Loans - Fixed |

1.69 |

18,074.89 |

305.18 |

|

DM Loans - Variable |

0.06 |

2,355.39 |

1.38 |

|

Vishmitha/Cash Back |

1.48 |

2,182.42 |

32.32 |

|

Housing Loans - Fixed |

2.78 |

6,460.92 |

179.57 |

|

Housing Loans - Variable |

0.07 |

3,588.09 |

2.47 |

|

Staff loans |

2.08 |

2,420.59 |

50.39 |

|

Pawning |

0.52 |

171.24 |

0.88 |

|

AF Lease |

1.25 |

15,043.09 |

188.31 |

|

AF Loans |

1.76 |

3,390.24 |

59.52 |

|

Hire Purchase |

0.61 |

291.32 |

1.77 |

|

IB Loans - LKR |

1.23 |

3,566.30 |

43.80 |

|

Deposits Placed - LKR |

0.00 |

75.00 |

0.00 |

|

Investments in T Bills HTM |

0.00 |

- |

- |

|

Investments in T Bonds HTM |

1.85 |

721.60 |

13.33 |

|

Investments in T Bills Trading |

0.09 |

746.14 |

0.70 |

|

Investments in T Bonds Trading |

0.94 |

454.58 |

4.26 |

|

Investments in Bills & Bonds AFS |

1.02 |

50,814.17 |

520.67 |

|

Investment in Debentures |

0.31 |

2,675.61 |

8.31 |

|

Reverse Repos |

0.00 |

- |

- |

|

Total Assets |

260,627.72 |

3,147.19 |

|

|

Liabilities: |

|

|

|

|

Demand Deposits - LKR |

1.51 |

17,370.81 |

261.79 |

|

Savings Deposits - LKR |

3.05 |

26,367.80 |

804.99 |

|

Call Deposits - LKR |

2.94 |

1,297.64 |

38.16 |

|

Term Deposits - LKR |

0.38 |

169,204.70 |

642.55 |

|

Margin Deposits - LKR |

3.09 |

585.00 |

18.09 |

|

Repurchase Agreements |

0.09 |

8,637.23 |

7.53 |

|

Money Market - LKR |

0.00 |

75.70 |

0.00 |

|

Institutional Borrowing - LKR |

0.00 |

- |

- |

|

Credit Lines - Fixed |

3.29 |

5,513.85 |

181.47 |

|

Credit Lines - Variable |

0.06 |

2,686.45 |

1.48 |

|

Debentures |

3.28 |

19,410.50 |

636.49 |

|

Equity & Other Liabilities |

2.65 |

9,478.04 |

251.17 |

|

Total Liabilities |

260,627.72 |

2,843.73 |

|

|

Price Sensitivity |

|

|

303.46 |

|

Limit |

1,000 |

Modified Duration - measurement of the portfolio to a 1% change in interest rates

Price Sensitivity - Sum of value change in each portfolio due to a 1% change in interest rates

Source - Fiserve ALM System

The Equity price risk arises due to adverse movement in the value of the individual stock price or of the corresponding equity index. Bank does not engage in equity trading at present but the investments held in the AFS portfolio are subject to mark to market valuation.

Equity Position Risk Measurements

|

|

Held for Trading LKR .000 |

Available for sale |

|

|

Impact on statement of Profit or Loss |

Impact on Other Comprehensive Income |

|

Shock of 15% on Equity price |

204,977 |

LKR 000'

|

TYPE |

Carrying Value |

Fair Value |

Realized gains/losses |

Unrealized gains/ losses |

Amount included in capital adequacy calculation |

|

|

Amount adjusted from CET 1 capital |

Amount considered for Market Risk |

|||||

|

Available for sale -AFS |

1,659,702 |

1,381,658 |

- |

(278,044) |

1,122,016 |

259,642 |

Commodity price risk arises due to volatilities in the commodity exposure of the Bank. The Bank was exposed to the Gold Buffer stock of the underlying product “Raththaran Ithurum” which was fully disposed during the year 2017.

Counterparty RiskWhen undertaking foreign exchange dealing and trading with interbank counterparties and corporates, two general types of risks arise.

-

Pre-settlement Risk - Refers to the counterpart becoming insolvent prior to the settlement date of transaction. The exposure comes by way of banks’ inability to find an alternate party to deal on same rates (interest or exchange) due to market changes.

-

Settlement Risk - Relates to the event where the counterpart to the deal is unable to honour settlement obligations (either in local currency or foreign currency) to the bank after having taken possession of funds paid by the bank in settlement.

The Bank set individual counterpart limits to mitigate such risk. These limits are set through critically assessing the financial standing, balance sheet size and other risk parameters of such counterparts.

LIQUIDITY RISK

Liquidity risk is the risk that the Bank is unable to meet its financial obligations in a timely manner without incurring unacceptable losses. Financial obligations include liabilities to depositors, payments due under derivative contracts, settlement of securities borrowings and repurchase transactions, lending and investment commitments.

Effective liquidity risk management is essential to maintain the confidence of depositors and counterparties as well as to ensure that the Bank’s core businesses continue to generate revenue, even under stressed conditions.

Objective of Liquidity Risk Management

The objective of our liquidity framework is to ensure that all anticipated funding commitments can be met when due and allow us to withstand liquidity stresses whilst maintaining our business profile. It is designed to be adaptable to changing business models, markets and regulations. The Bank continues to focus on liability generation, which will be a necessary pre-condition for significant asset growth.

Policy Framework

The Bank maintains well-articulated liquidity risk management policies and procedures, which drive the level of liquidity risk exposures and determine the business size and maturities which ensure that it has at all times sufficient liquidity to meet its financial obligations at a fair market price. Also the Bank monitors key liquidity metrics on a regular basis, both on local currency and foreign currency balance sheets and prudential limits are set to better manage the liquidity profile of the Bank.

Process

The responsibility for the Liquidity risk management of the Bank rests with the ALCO. Bank’s Treasury/ALM units are responsible for executing the day-to-day liquidity management of the Bank within the parameters set by ALCO. Key liquidity measures are managed and monitored on a daily, weekly or monthly basis to ensure that the Bank meets the regulatory (Liquid Asset Ratio, Statutory Reserve Requirement and Liquidity Coverage Ratio) as well as the internal limits whilst meeting the customer demands without incurring unacceptable losses.

In this context, MRMO circulates Reports on Open exposure levels, Liquidity risk exposures, ALM and liquidity risk assessment to the Management/Board on a regular basis.

Liquidity Risk Governance structure

The Bank is equipped with a comprehensive Liquidity Contingency Funding Plan (LCFP) linked to the Business Continuity Plan, which is in line with the regulatory guidelines. The LCFP clearly defines the responsibilities of the Liquidity Management Team, Internal/external liquidity risk trigger points, stage for plan invocation/de-activation and the action plans to be exercised to ensure that all stakeholders of the Bank are safeguarded. We have also entered into reciprocal liquidity funding agreements with identified counterpart banks to ensure stability.

Liquidity Risk AnalyticsLiquidity measurement could be measured through Stock approach or Flow approach. Under the stock approach liquidity is measured in terms of key ratios which portray the liquidity stored in the balance sheet. In the flow approach a statement of maturities of assets and liabilities is prepared placing all cash flows in time bands according to the residual time to maturity. Separate gap limits are set for the local currency and foreign currency maturity mismatch reports based on the size and the nature of the Bank’s balance sheet.

Bank uses several internal prudential measures to manage its liquidity position, whilst meeting the regulatory limit. Certain limits are set for key liquidity measures, above the regulatory limit to give early warnings signals of tightening liquidity positions of the Bank. Factors such as market liquidity, exposure to interbank market, movement on loans and advances, deposit mix will be regularly monitored to identify any impending liquidity strain on the Bank.