ECONOMIC AND INDUSTRY ENVIRONMENT

What we have

achieved

GLOBAL ECONOMY

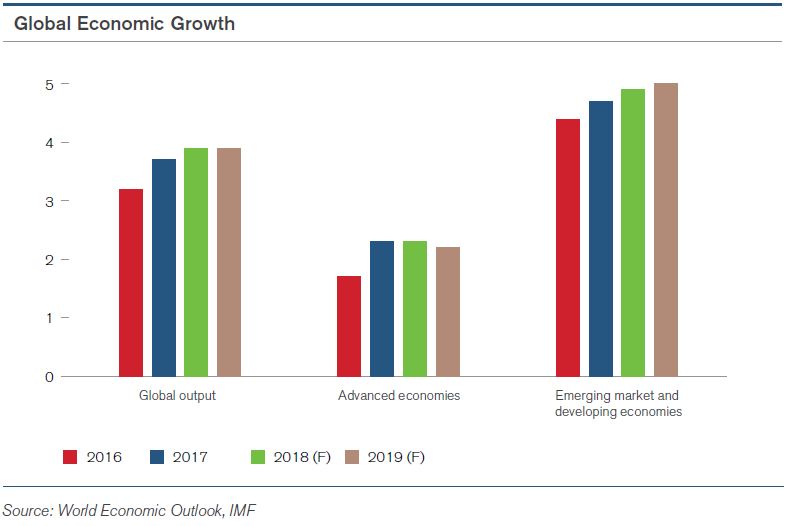

Global economic activity firmed up in 2017 with output estimated to have expanded by 3.7% during the year. World trade improved in the 3rd quarter supported by the better sentiments and investments in advanced economies and increased manufacturing in Asia. Crude oil prices rose to over USD 60 a barrel from around USD 54 at the beginning of the year, reflecting improving global demand and an OPEC agreement to limit production. This, in turn, resulted in an up-tick in inflation and increases in overall commodity prices. Capital inflows to emerging economies remained resilient supporting broad-based growth.

Global growth is expected to pick up pace to 3.9% in 2018 and 2019 with advanced economies growth exceeding 2% while Emerging & Developing Asia is expected to maintain its growth rate of 6.5%. Downside risks to this projection include the escalation of geopolitical tensions and adoption of nationalistic and inward looking policies.

SRI LANKAN ECONOMY

Sri Lanka’s economic growth was lower than anticipated in 2017, with unfavourable weather conditions, a tighter fiscal policy stance and global headwinds impacting overall growth. Despite these challenges, progress was made on the policy front with economic reforms targeted towards fiscal consolidation, attracting foreign direct investment and stabilizing macro-economic fundamentals expected to bear fruition over the medium to long term. During the first 9 months of 2017, the country’s GDP grew at 3.7% supported by moderate expansion of the services and industry sectors while the agriculture sector had a negative impact. Inclement weather conditions primarily affected the agriculture sector (which contracted by 3.2% in the first 9 months) although spill-over effects were felt across other sectors of the economy. Industry sector grew by 4.5%, led by the continued expansion in construction, mining and quarry activities. The services sector grew by 4.2%, upheld by financial services, wholesale and retail trade activities and transportation.

The Central Bank of Sri Lanka maintained a relatively tight monetary policy stance during most part of the year with a view to addressing inflationary pressures. Accordingly, the policy rate was raised by 25 bps in March 2017, resulting in the Standing Deposit Facility Rate (SDFR) and the Standard Lending Facility Rate (SLFR) increasing to 7.25% and 8.75% respectively. Resultantly, market interest rates moved up during the first half of the year, with commercial banks’ deposit and lending rates also increasing. However, liquidity improvements in the domestic money market during the second half of 2017 resulted in market interest rates tapering off towards the latter part of 2017.

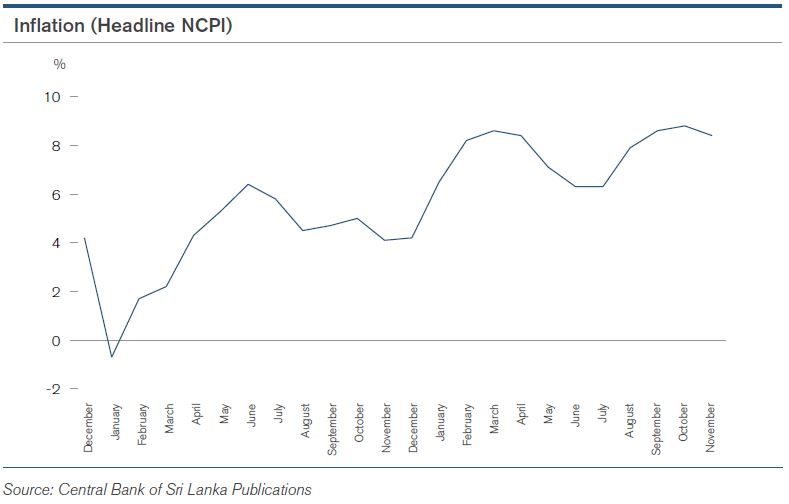

Inflationary pressures were felt during most part of the year, stemming from tax revisions, rising international commodity prices as well as supply constraints of domestic produce amidst inclement weather conditions. Volatilities in food inflation were reflected in the Headline National Consumers’ Price Index (NCPI) which fluctuated between 6.3% and 8.8% (y-o-y) during the year. The CBSL plans to move to a Flexible Inflation Targeting (FIT) regime, over the medium term enabling a low inflation environment to be sustained underpinned by a strong fiscal position, effective monetary policy and regulator credibility.

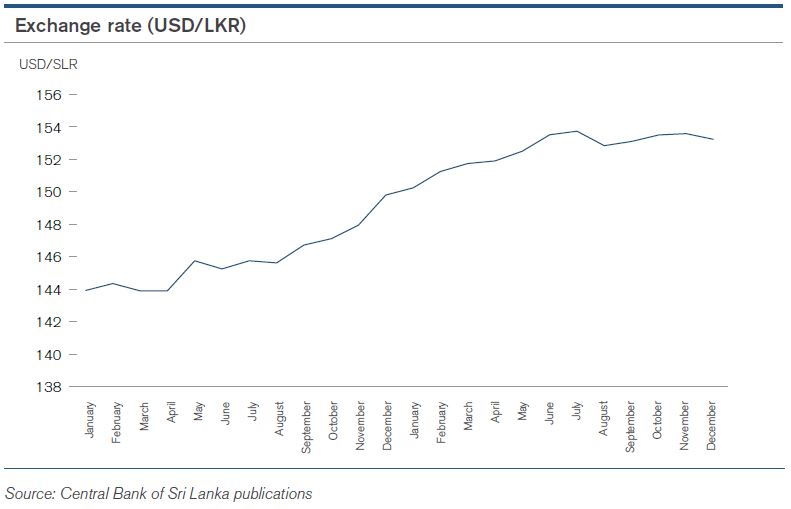

Export earnings strengthened in 2017 following the recovery in key export markets, increased commodity prices in international markets, the restoration of GSP+ concessions from the European Market as well as institutional support in encouraging exports. Imports also increased due to higher fuel imports and the Government being compelled to encourage the import of rice to bridge the prevalent supply shortfall. Overall, the trade deficit widened by 8% during the year. The CBSL sought to allow more flexibility in the exchange rate, with market forces being allowed to determine the rate. Emphasis was also placed on absorbing foreign exchange from the domestic interbank market to build up forex reserves and smoothen out rate fluctuations. The Rupee faced some downward pressure in the first quarter of the year, however conditions improved thereafter following foreign investments into the capital and government securities market. Sri Lanka also received the third and fourth tranches of the Extended Fund Facility from the IMF during the year, demonstrating the successful achievement of specific performance criteria. Overall, the Sri Lankan Rupee depreciated by 2.0% against the US Dollar during the year while gross official reserves increased to USD 8.0 billion from USD 6.0 billion as at end-2016.

Outlook

Although the country’s tighter monetary and fiscal policy could affect headline growth over the short-term, it is expected to lay a firm foundation for sustainable and longterm economic development. Broad-based reforms targeted towards fiscal consolidation, development of a cohesive export strategy and a renewed drive to attract foreign investments has positioned the country for strong growth, although political will and commitment will be crucial in implementing reforms and achieving the country’s growth potential.

THE BANKING SECTOR

Sri Lanka’s banking sector consists of 13 local and 12 international licensed commercial banks (LCB) and 7 licensed specialized banks (LSB). These institutions have been classified as large, medium and small banks based on their asset base, with the top 6 banks (assets over LKR 500 billion) holding a dominant share of assets, loans and advances and deposits. The sector collectively operates a network of over 3,500 branches islandwide and plays a critical role in fostering economic growth, facilitating transactions and mobilizing deposits. With the Government’s regional development agenda, the banking sector is expected to play an important role in enhancing financial inclusion and providing access to affordable financial solutions across the country.

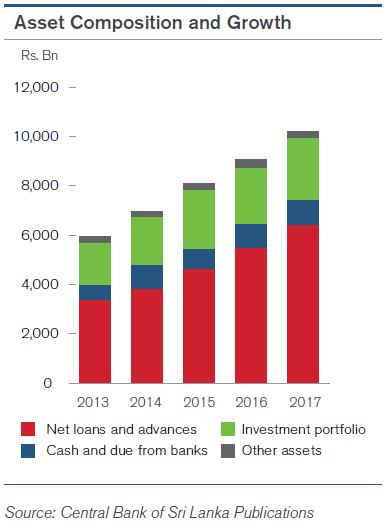

Growth: The sector’s asset base recorded a YoY growth of 13.8% in 2017 (compared to 15.4% in 2016) supported by credit and investment portfolio expansion. Despite the relatively higher interest rates, the advances portfolio expanded by 16.1% during the same period, supported by increased lending towards consumption, trading, manufacturing and tourism sectors. Portfolio growth was funded primarily through public deposits. The Sector’s asset composition remained relatively unchanged with credits assets accounting for around 62% of the total asset base followed by Investments (25%) and other assets.

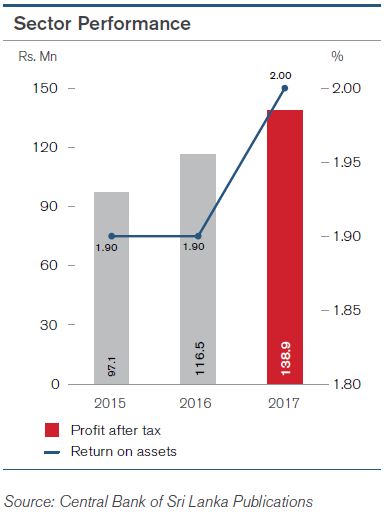

Performance: The Sector achieved strong growth in profits with profit after tax increasing by 19% to LKR 138.9 billion in 2017. Performance was upheld by strong growth in net interest income, significant capital gains and better cost efficiencies. The Sector’s Return on Assets (ROA) and Return on Equity (ROE) clocked in at 2.0% and 17.6% respectively during the reviewed period (compared to 1.9% and 17.3% in the corresponding period of 2016)

Asset quality: The quality of the Sector’s loan portfolio deteriorated marginally during the period under review with an influx of non-performing-loans from the agriculture, tourism and manufacturing sectors. Despite an increase in absolute NPLs, the gross NPL ratio declined to 2.5% in 2017, from 2.7% the year before. Total provision coverage amounted to 69.8% during the year.

Funding: Deposits continue to be the main funding source of the sector accounting for around 70% of total assets. The relatively high interest rates during the first half of the year resulted in an influx of deposits to the sector, with total deposits increasing by 17.4% during the year. The growth stemmed primarily from term deposits; meanwhile the sector’s CASA ratio declined further to 34.2% in 2017, from 34.5% in 2016.

The sector’s exposure to borrowings declined during the year. Total borrowings decelerated by 5.3% mainly due to a fall in rupee borrowings. Foreign currency borrowings however increased marginally mainly from domestic sources while borrowings from foreign sources declined during the period under review.

Capitalization: The Sector’s capital cushioning remained adequate, although declining marginally in view of the strong loan expansion. The Tier 1 Risk Weighted Capital Adequacy Ratio (RWCAR) and Overall RWCAR declined to 12.3% and 15.2% respectively, compared to 12.6% and 15.6% in 2016.

Outlook

The CBSL intends to introduce several policy reforms aimed at strengthening the regulatory and supervisory framework governing financial institutions. Key among these are the implementation of the Basel III minimum capital requirements, following which, banks are required to enhance their high-quality capital. Meanwhile, with the adoption of SLFRS 9- Financial Instruments banks will be required to recognise credit losses under the expected loss approach instead of the existing incurred loan loss approach. This will require banks to further enhance their capital buffers, improving the sector’s ability to absorb shocks and contributing to the overall stability of the sector. With regards to performance, the current monetary policy stance is expected to result in the gradual deceleration of loan growth and banks will be compelled to strengthen their risk management practices to ensure that portfolio quality is maintained.